8 Classification

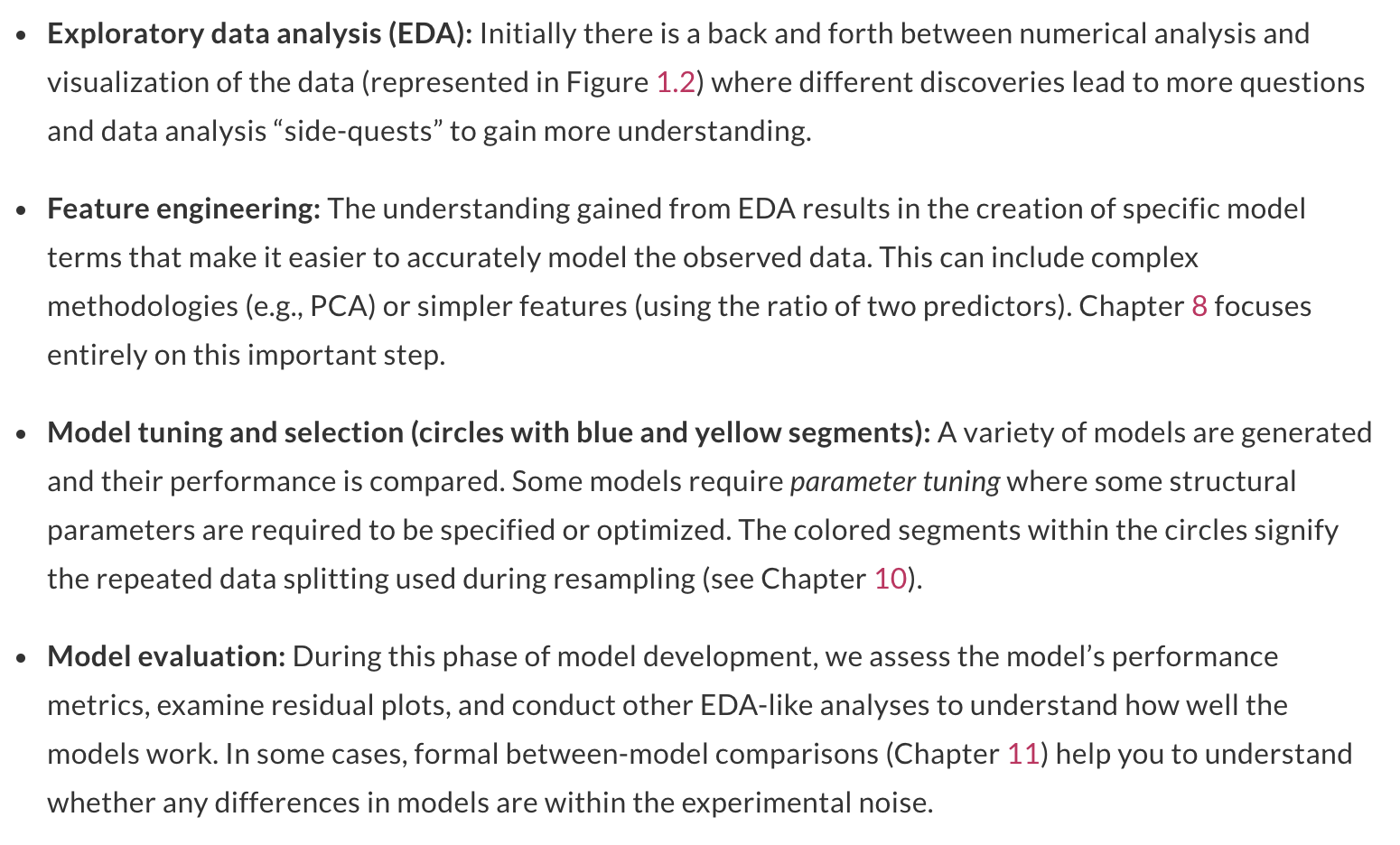

Baumer (2015) provides a concise explanation of how both statistics and data science work to enhance ideas of machine learning, one aspect of which is classification:

In order to understand machine learning, one must recognize the differences between the mindset of the data miner and the statistician, notably characterized by Breiman (2001), who distinguished two types of models f for y, the response variable, and x, a vector of explanatory variables. One might consider a data model f such that y \(\sim\) f(x), assess whether f could reasonably have been the process that generated y from x, and then make inferences about f. The goal here is to learn about the real process that generated y from x.

Alternatively, one might construct an algorithmic model f, such that \(y \sim f(x)\), and use f to predict unobserved values of y. If it can be determined that f does in fact do a good job of predicting values of y, one might not care to learn much about f. In the former case, since we want to learn about f, a simpler model may be preferred. Conversely, in the latter case, since we want to predict new values of y, we may be indifferent to model complexity (other than concerns about overfitting and scalability).

Classification is a supervised learning technique to extract general patterns from the data in order to build a predictor for a new test or validation data set. That is, the model should classify new points into groups (or with a numerical response values) based on a model built from a set of data which provides known group membership for each value. We will consider classifying into categories (often only one of two categories) as well as predicting a numeric variable (e.g., support vector machines and linear regression).

Some examples of classification techniques include: linear regression, logistic regression, neural networks, classification trees, Random Forests, k-nearest neighbors, support vector machines, näive Bayes, and linear discriminant analysis. We will cover the methods in bold.

Simple is Better (From Fielding (2007), p. 87)

- We want to avoid over-fitting the model (certainly, it is a bad idea to model the noise!)

- Future prediction performance goes down with too many predictors.

- Simple models provide better insight into causality and specific associations.

- Fewer predictors implies fewer variables to collect in later studies.

That said, the model should still represent the complexity of the data! We describe the trade-off above as the “bias-variance” trade-off. In order to fully understand that trade-off, let’s first cover the structure of model building and also the classification method known as \(k\)-Nearest Neighbors.

8.1 Model Building Process

All classification and prediction models have the same basic steps. The data is preprocessed, the model is trained, and then the model is validated.

If the variables and information used to train the model has not been fully tuned, processed, and considered for the model, it won’t matter how sophisticated or special the model is. Garbage in, garbage out.

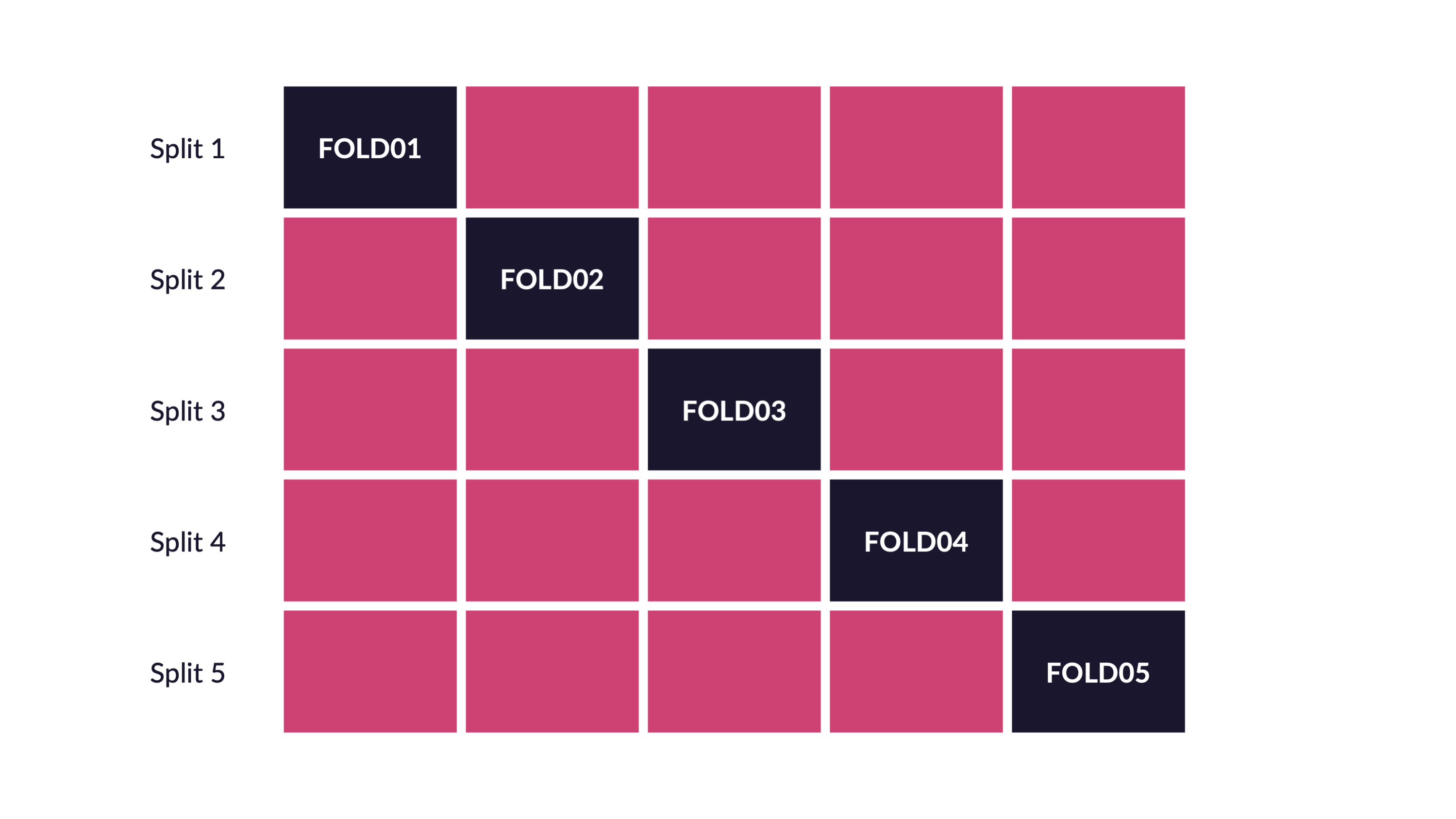

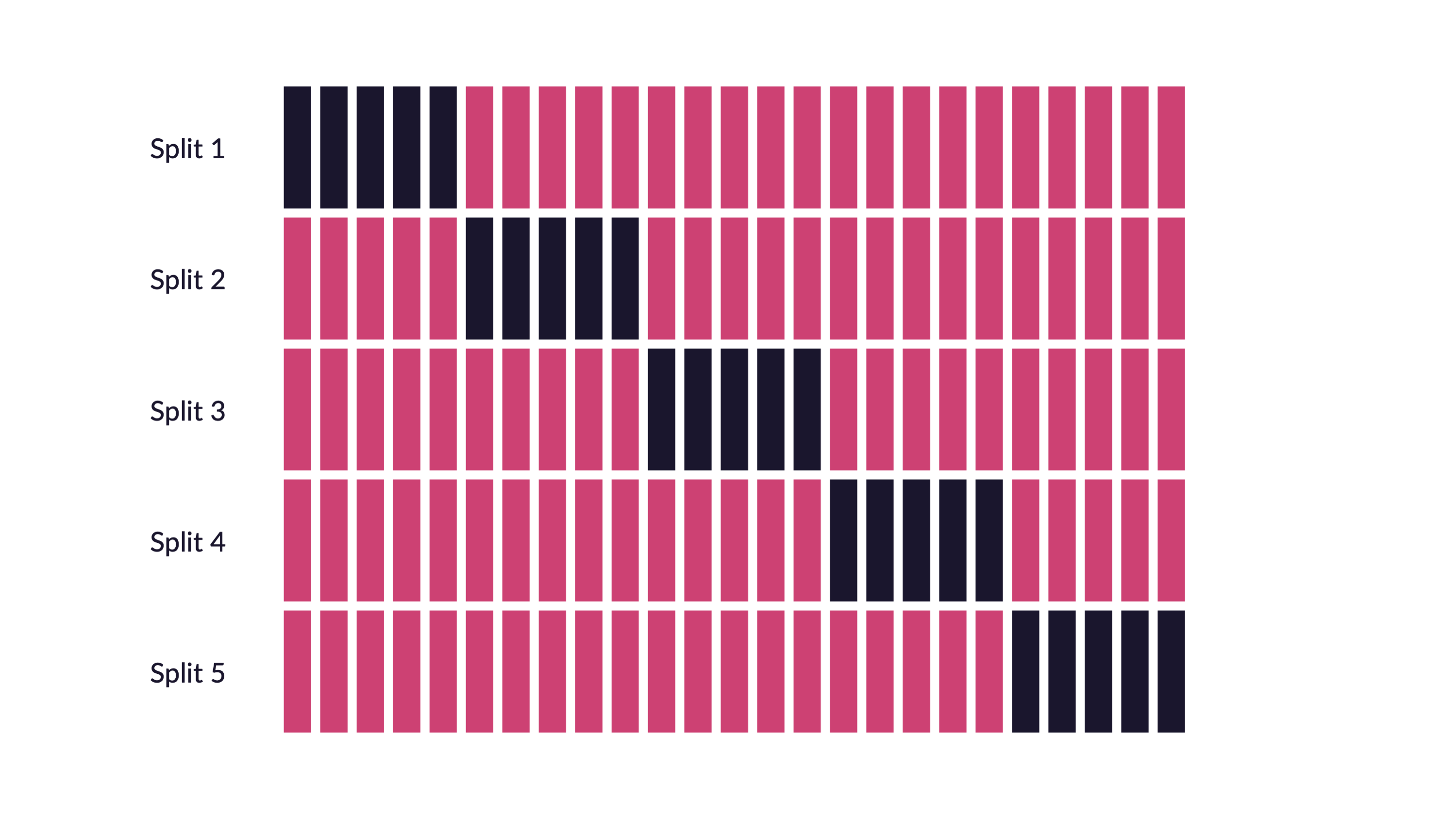

8.1.1 Cross Validation

Bias-variance trade-off

Excellent resource

for explaining the bias-variance trade-off: http://scott.fortmann-roe.com/docs/BiasVariance.html

Variance refers to the amount by which \(\hat{f}\) would change if we estimated it using a different training set. Generally, the closer the model fits the data, the more variable it will be (it’ll be different for each data set!). A model with many many explanatory variables will often fit the data too closely.

Bias refers to the error that is introduced by approximating the “truth” by a model which is too simple. For example, we often use linear models to describe complex relationships, but it is unlikely that any real life situation actually has a true linear model. However, if the true relationship is close to linear, then the linear model will have a low bias.

Generally, the simpler the model, the lower the variance. The more complicated the model, the lower the bias. In this class, cross validation will be used to assess model fit. [If time permits, Receiver Operating Characteristic (ROC) curves will also be covered.]

\[\begin{align} \mbox{prediction error } = \mbox{ irreducible error } + \mbox{ bias } + \mbox{ variance} \end{align}\]

- irreducible error The irreducible error is the natural variability that comes with observations. No matter how good the model is, we will never be able to predict perfectly.

- bias The bias of the model represents the difference between the true model and a model which is too simple. That is, the more complicated the model (e.g., smaller \(k\) in \(k\)NN), the closer the points are to the prediction. As the model gets more complicated (e.g., as \(k\) decreases), the bias goes down.

- variance The variance represents the variability of the model from sample to sample. That is, a simple model (big \(k\) in \(k\)NN) would not change a lot from sample to sample. The variance decreases as the model becomes more simple (e.g., as \(k\) increases).

Note the bias-variance trade-off. We want our prediction error to be small, so we choose a model that is medium with respect to both bias and variance. We cannot control the irreducible error.

![Test and training error as a function of model complexity. Note that the error goes down monotonically only for the training data. Be careful not to overfit!! [@ESL]](figs/varbias.png)

Figure 1.4: Test and training error as a function of model complexity. Note that the error goes down monotonically only for the training data. Be careful not to overfit!! (Hastie, Tibshirani, and Friedman 2001)

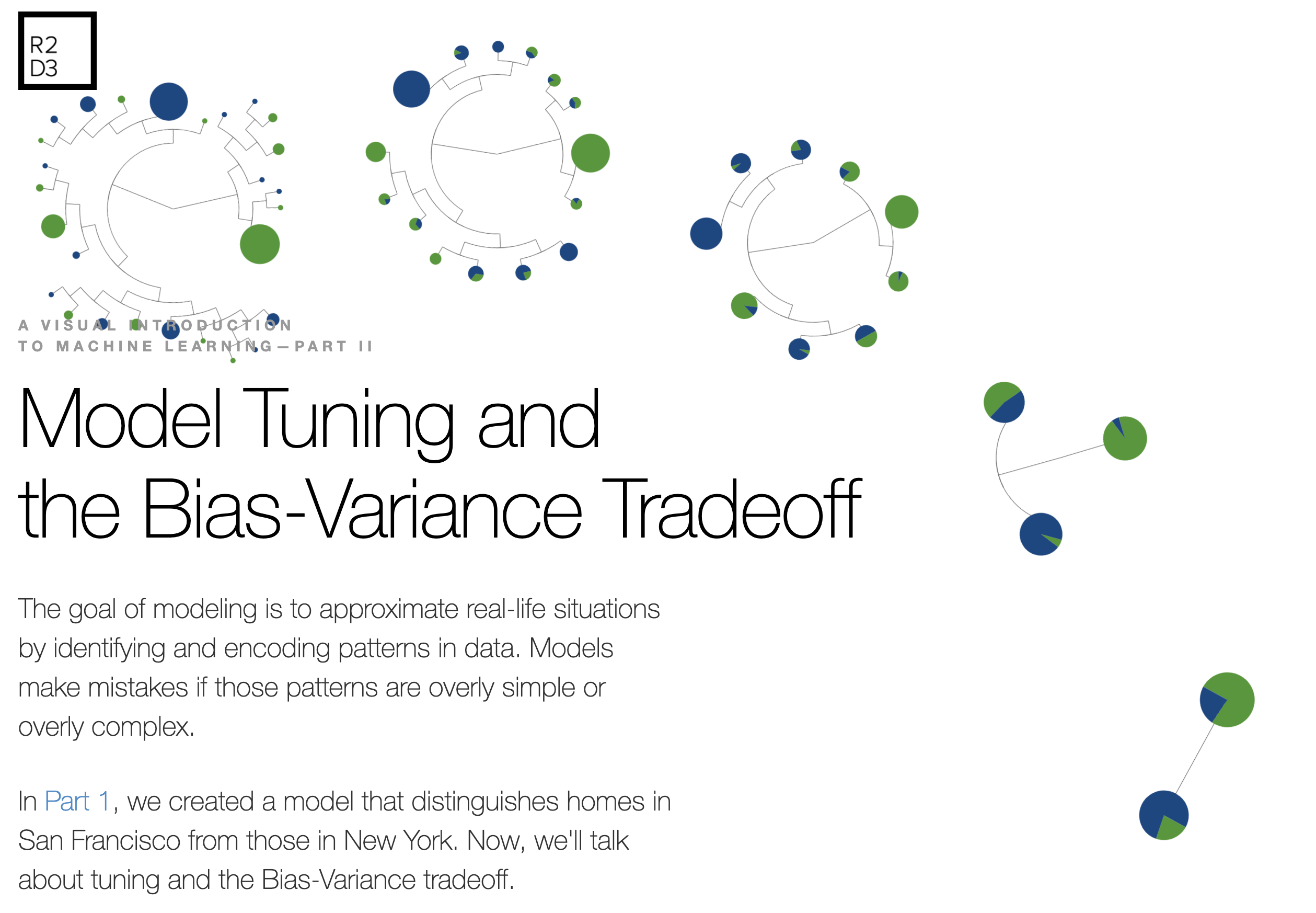

The following interactive visualization does an excellent job of communicating the trade-off between bias and variance as a function of a specific tuning parameter, here: minimum node size of a classification tree. http://www.r2d3.us/visual-intro-to-machine-learning-part-2/

Figure 1.5: Great interactive viz at http://www.r2d3.us/visual-intro-to-machine-learning-part-2/

Implementing Cross Validation

![[@flach12]](figs/overfitting.jpg)

Figure 1.6: (Flach 2012)

Cross validation is typically used in two ways.

- To assess a model’s accuracy (model assessment).

- To build a model (model selection).

Different ways to CV

Suppose that we build a classifier on a given data set. We’d like to know how well the model classifies observations, but if we test on the samples at hand, the error rate will be much lower than the model’s inherent accuracy rate. Instead, we’d like to predict new observations that were not used to create the model. There are various ways of creating test or validation sets of data:

- one training set, one test set [two drawbacks: estimate of error is highly variable because it depends on which points go into the training set; and because the training data set is smaller than the full data set, the error rate is biased in such a way that it overestimates the actual error rate of the modeling technique.]

- leave one out cross validation (LOOCV)

- remove one observation

- build the model using the remaining n-1 points

- predict class membership for the observation which was removed

- repeat by removing each observation one at a time

-

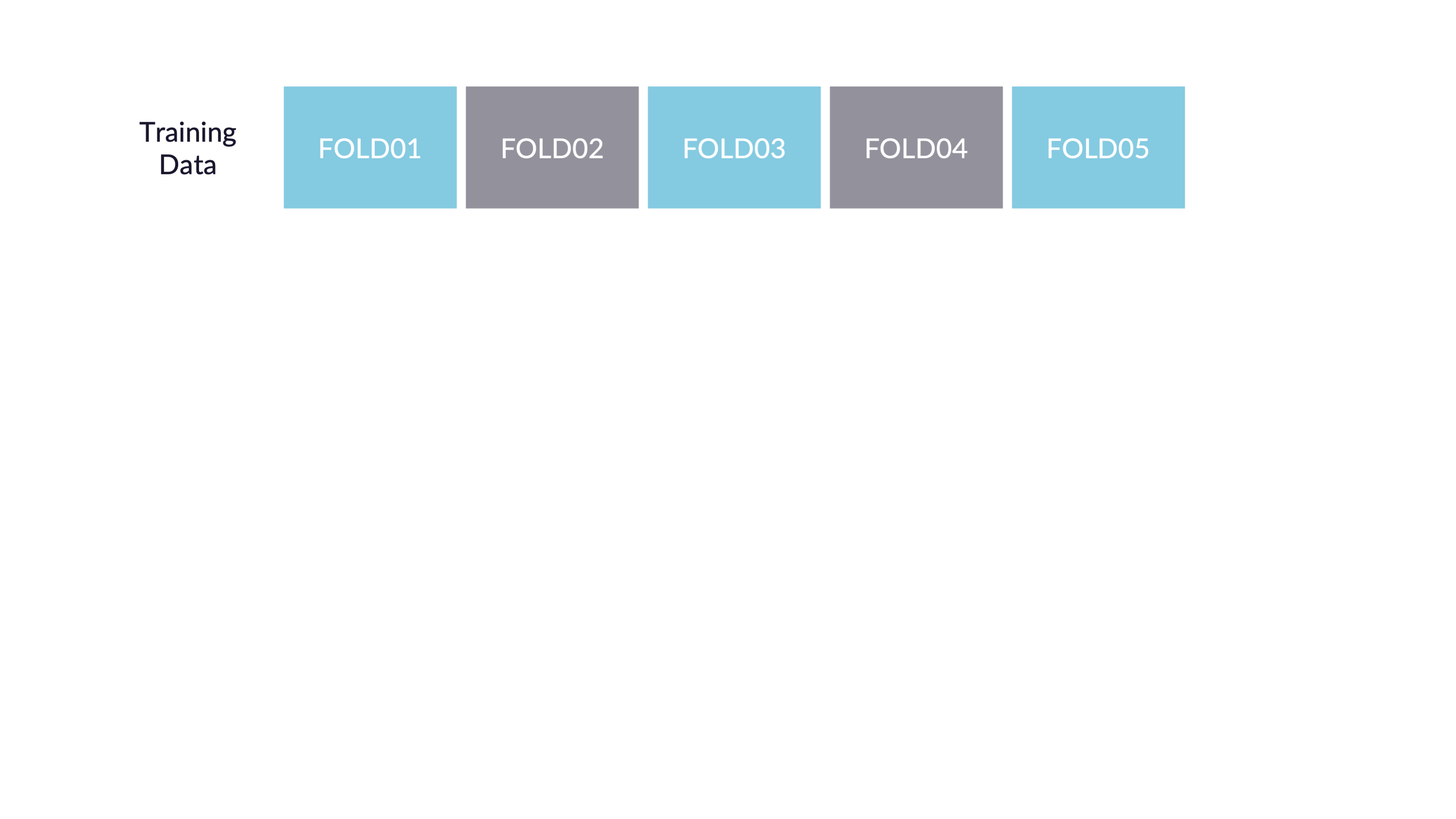

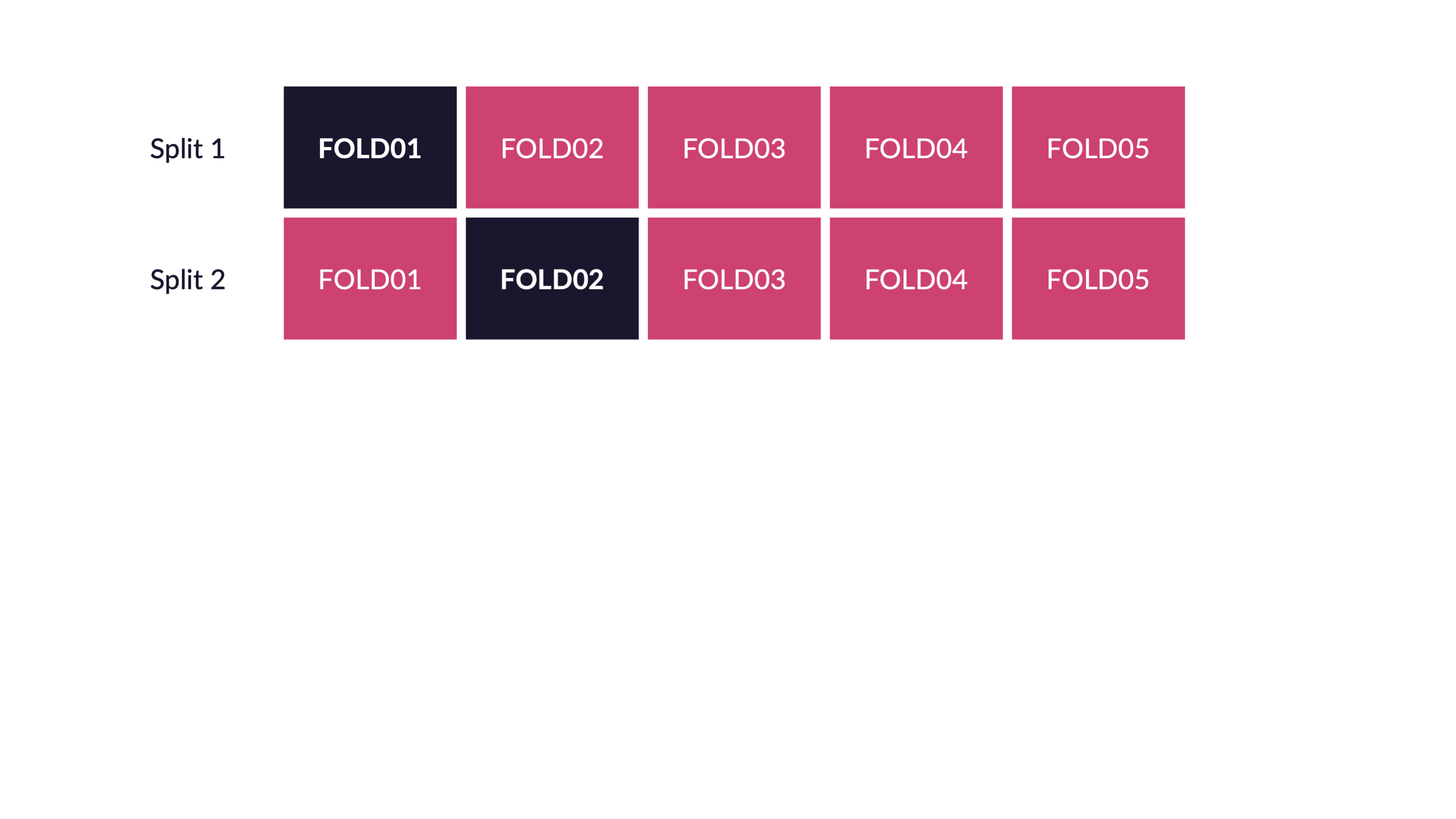

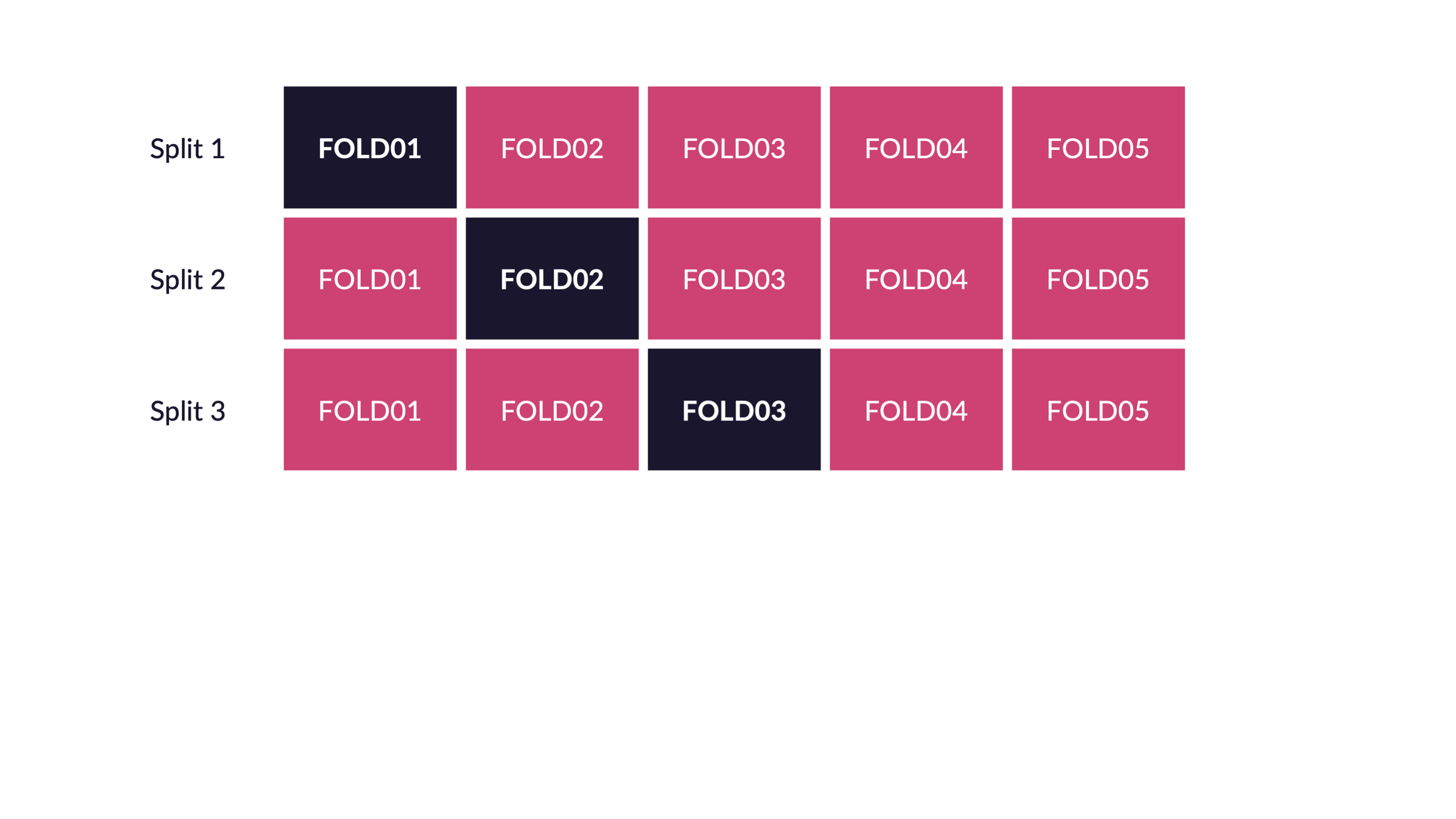

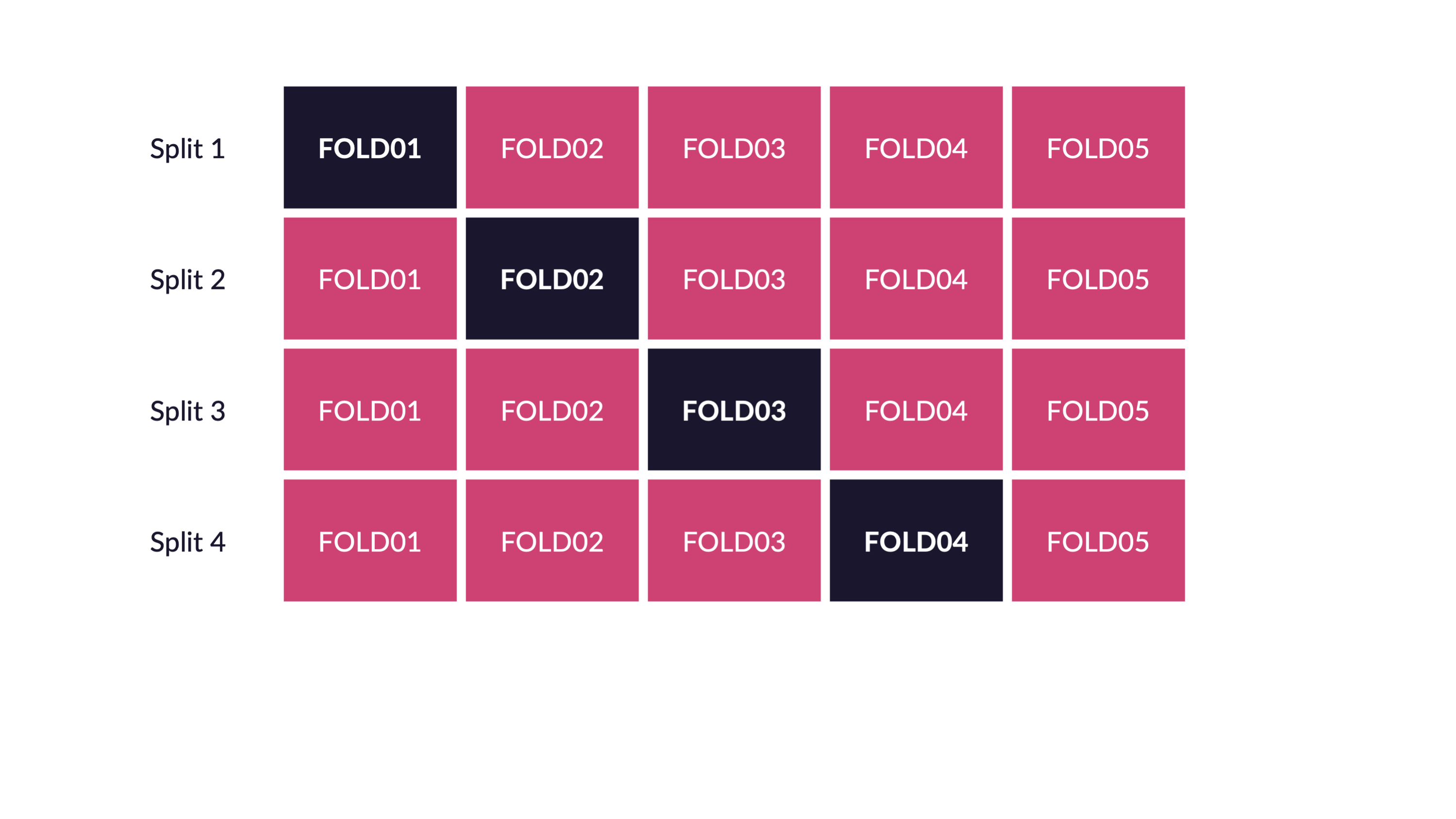

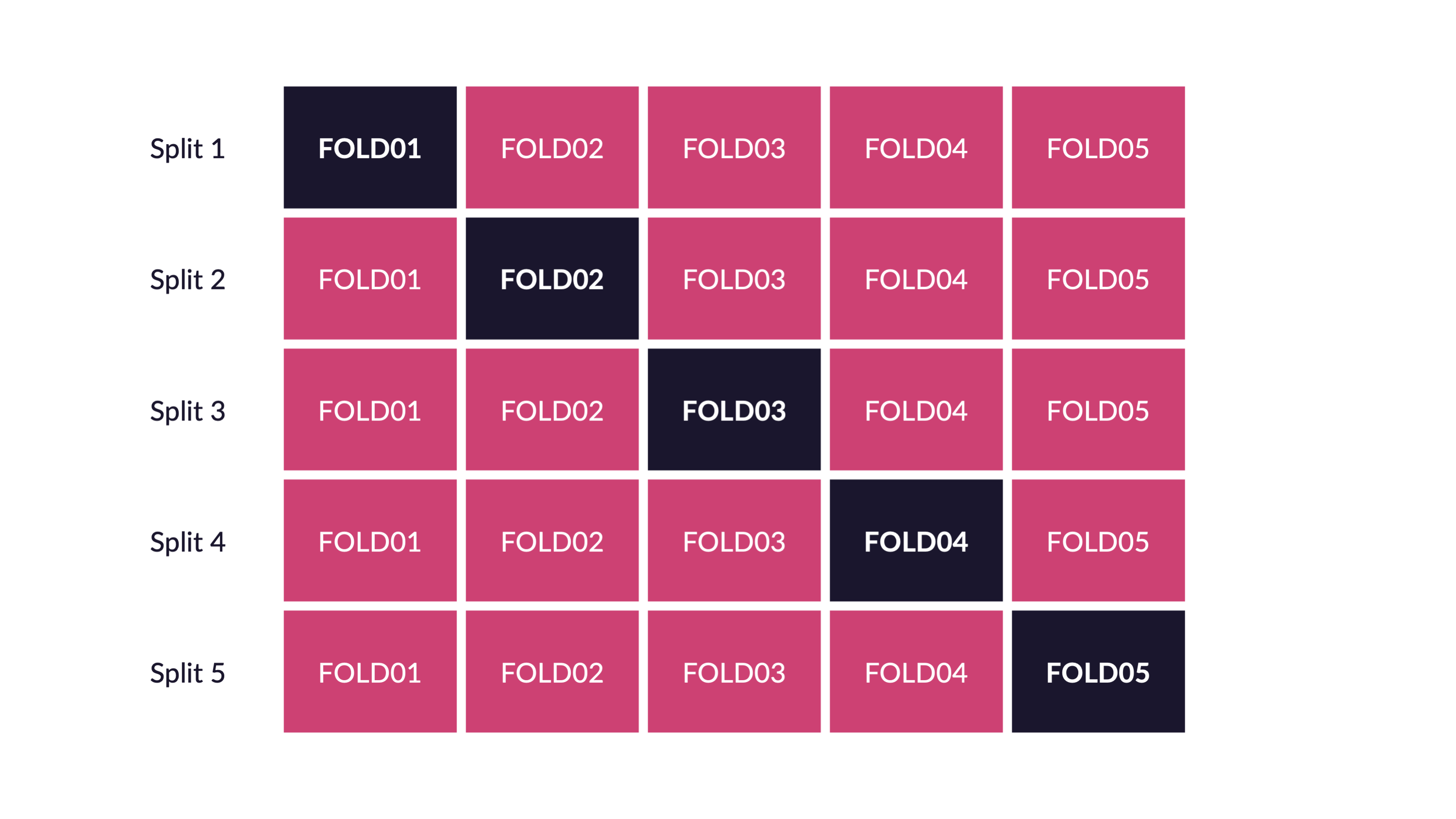

\(V\)-fold cross validation (\(V\)-fold CV)

- like LOOCV except that the algorithm is run \(V\) times on each group (of approximately equal size) from a partition of the data set.]

- LOOCV is a special case of \(V\)-fold CV with \(V=n\)

- advantage of \(V\)-fold is computational

- \(V\)-fold often has a better bias-variance trade-off [bias is lower with LOOCV. however, because LOOCV predicts \(n\) observations from \(n\) models which are basically the same, the variability will be higher (i.e., based on the \(n\) data values). with \(V\)-fold, prediction is on \(n\) values from \(V\) models which are much less correlated. the effect is to average out the predicted values in such a way that there will be less variability from data set to data set.]

CV for Model assessment 10-fold

- assume \(k\) is given for \(k\)-NN

- remove 10% of the data

- build the model using the remaining 90%

- predict class membership / continuous response for the 10% of the observations which were removed

- repeat by removing each decile one at a time

- a good measure of the model’s ability to predict is the error rate associated with the predictions on the data which have been independently predicted

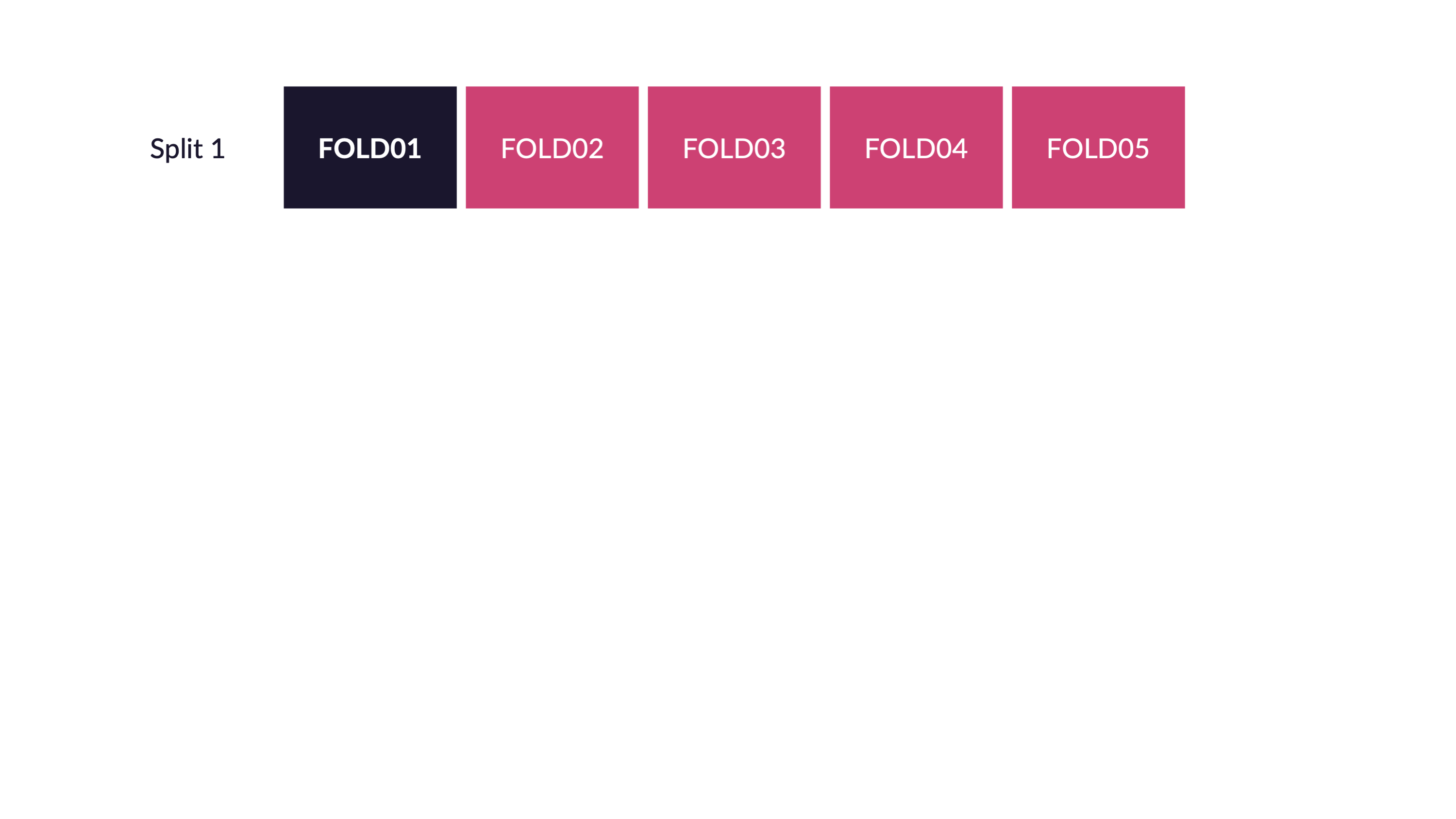

CV for Model selection 10-fold

- set \(k\) in \(k\)-NN

- build the model using the \(k\) value set above:

- remove 10% of the data

- build the model using the remaining 90%

- predict class membership / continuous response for the 10% of the observations which were removed

- repeat by removing each decile one at a time

- measure the CV prediction error for the \(k\) value at hand

- repeat steps 1-3 and choose the \(k\) for which the prediction error is lowest

CV for Model assessment and selection 10-fold

To do both, one approach is to use test/training data and CV in order to both model assessment and selection. Note that CV could be used in both steps, but the algorithm is slightly more complicated.

- split the data into training and test observations

- set \(k\) in \(k\)-NN

- build the model using the \(k\) value set above on only the training data:

- remove 10% of the training data

- build the model using the remaining 90% of the training data

- predict class membership / continuous response for the 10% of the training observations which were removed

- repeat by removing each decile one at a time from the training data

- measure the CV prediction error for the \(k\) value at hand on the training data

- repeat steps 2-4 and choose the \(k\) for which the prediction error is lowest for the training data

- using the \(k\) value given in step 5, assess the prediction error on the test data

![Nested cross-validation: two cross-validation loops are run one inside the other. [@CVpaper]](figs/CV.jpg)

Figure 7.1: Nested cross-validation: two cross-validation loops are run one inside the other. (Varoquaux et al. 2017)

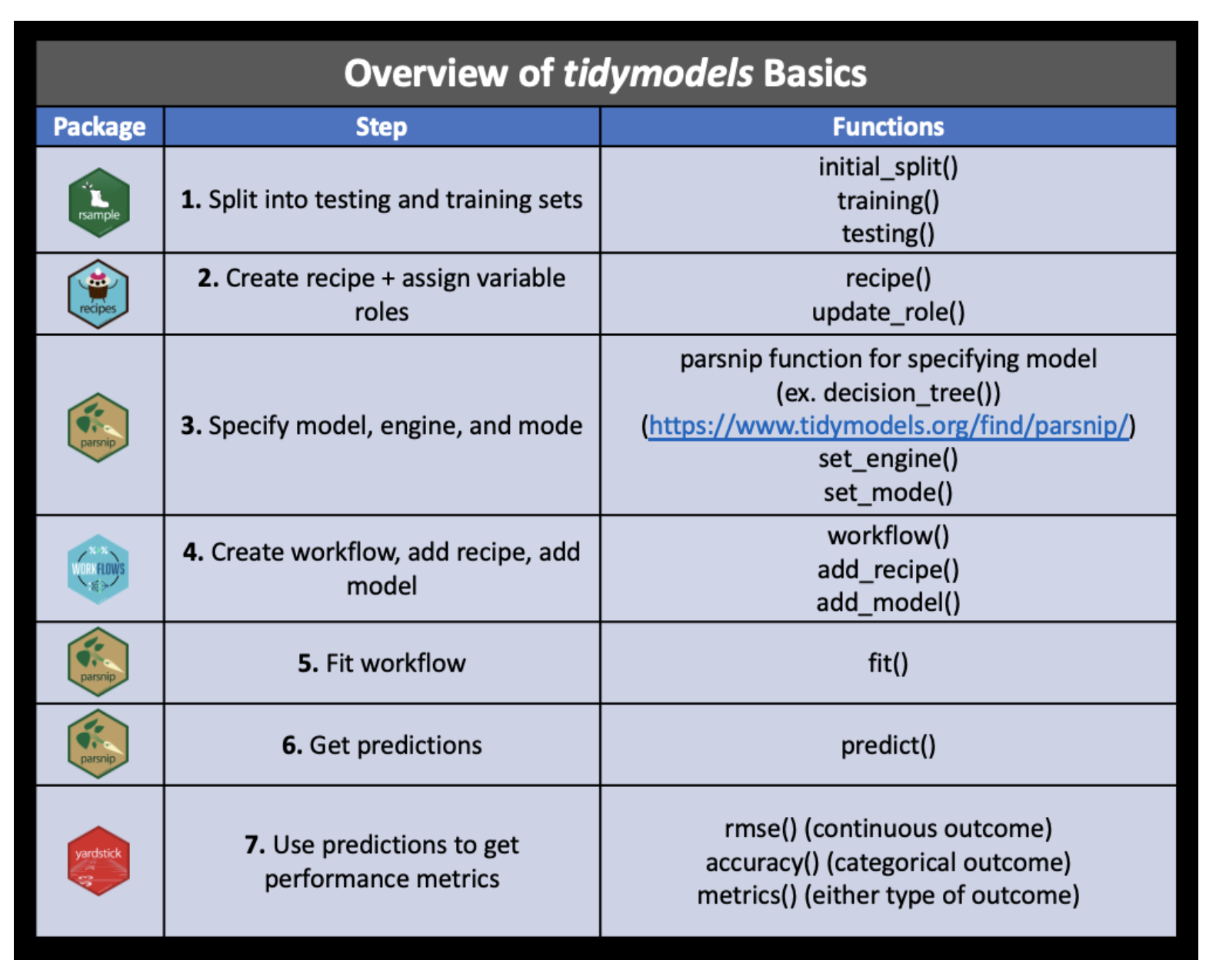

8.1.2 tidymodels

The tidymodels framework provides a series of steps that allow for systematic model building. The steps are:

- partition the data

- build a recipe

- select a model

- create a workflow

- fit the model

- validate the model

The process is synthesized in the following graphic from a course at Johns Hopkins, Tidyverse Skills for Data Science.

Figure 7.2: Image credit: Wright et al., Chapter 5 of Tidyverse Skills for Data Science https://jhudatascience.org/tidyversecourse/

1. Partition the data

Put the testing data in your pocket (keep it secret from R!!)

Figure 7.3: Image credit: Julia Silge

2. build a recipe

- Start the

recipe() - Define the variables involved

- Describe preprocessing step-by-step

feature engineering or preprocessing:

feature engineering is the process of transforming raw data into features (variables) that are better predictors (for the model at hand).

Examples include:

- create new variables (e.g., combine levels -> from state to region)

- transform variable (e.g., log, polar coordinates)

- continuous variables -> discrete (e.g., binning)

- numerical categorical data -> factors / character strings (one hot encoding)

- time -> discretized time

- missing values -> imputed

- NA -> level

- continuous variables -> center & scale (“normalize”)

step_ functions

For more information: https://recipes.tidymodels.org/reference/index.html

ls(pattern = '^step_', env = as.environment('package:recipes'))## [1] "step_arrange" "step_bagimpute"

## [3] "step_bin2factor" "step_BoxCox"

## [5] "step_bs" "step_center"

## [7] "step_classdist" "step_corr"

## [9] "step_count" "step_cut"

## [11] "step_date" "step_depth"

## [13] "step_discretize" "step_downsample"

## [15] "step_dummy" "step_dummy_extract"

## [17] "step_dummy_multi_choice" "step_factor2string"

## [19] "step_filter" "step_filter_missing"

## [21] "step_geodist" "step_harmonic"

## [23] "step_holiday" "step_hyperbolic"

## [25] "step_ica" "step_impute_bag"

## [27] "step_impute_knn" "step_impute_linear"

## [29] "step_impute_lower" "step_impute_mean"

## [31] "step_impute_median" "step_impute_mode"

## [33] "step_impute_roll" "step_indicate_na"

## [35] "step_integer" "step_interact"

## [37] "step_intercept" "step_inverse"

## [39] "step_invlogit" "step_isomap"

## [41] "step_knnimpute" "step_kpca"

## [43] "step_kpca_poly" "step_kpca_rbf"

## [45] "step_lag" "step_lincomb"

## [47] "step_log" "step_logit"

## [49] "step_lowerimpute" "step_meanimpute"

## [51] "step_medianimpute" "step_modeimpute"

## [53] "step_mutate" "step_mutate_at"

## [55] "step_naomit" "step_nnmf"

## [57] "step_nnmf_sparse" "step_normalize"

## [59] "step_novel" "step_ns"

## [61] "step_num2factor" "step_nzv"

## [63] "step_ordinalscore" "step_other"

## [65] "step_pca" "step_percentile"

## [67] "step_pls" "step_poly"

## [69] "step_profile" "step_range"

## [71] "step_ratio" "step_regex"

## [73] "step_relevel" "step_relu"

## [75] "step_rename" "step_rename_at"

## [77] "step_rm" "step_rollimpute"

## [79] "step_sample" "step_scale"

## [81] "step_select" "step_shuffle"

## [83] "step_slice" "step_spatialsign"

## [85] "step_sqrt" "step_string2factor"

## [87] "step_unknown" "step_unorder"

## [89] "step_upsample" "step_window"

## [91] "step_YeoJohnson" "step_zv"3. select a model

To specify a model:

- pick a model

- set the mode (regression vs classification, if needed)

- set the engine

Examples of engines for some of the classification algorithms we will cover in class:

show_engines("nearest_neighbor")## # A tibble: 2 × 2

## engine mode

## <chr> <chr>

## 1 kknn classification

## 2 kknn regression

show_engines("decision_tree")## # A tibble: 5 × 2

## engine mode

## <chr> <chr>

## 1 rpart classification

## 2 rpart regression

## 3 C5.0 classification

## 4 spark classification

## 5 spark regression

show_engines("rand_forest")## # A tibble: 6 × 2

## engine mode

## <chr> <chr>

## 1 ranger classification

## 2 ranger regression

## 3 randomForest classification

## 4 randomForest regression

## 5 spark classification

## 6 spark regression

show_engines("svm_poly")## # A tibble: 2 × 2

## engine mode

## <chr> <chr>

## 1 kernlab classification

## 2 kernlab regression

show_engines("svm_rbf")## # A tibble: 4 × 2

## engine mode

## <chr> <chr>

## 1 kernlab classification

## 2 kernlab regression

## 3 liquidSVM classification

## 4 liquidSVM regression

show_engines("linear_reg")## # A tibble: 7 × 2

## engine mode

## <chr> <chr>

## 1 lm regression

## 2 glm regression

## 3 glmnet regression

## 4 stan regression

## 5 spark regression

## 6 keras regression

## 7 brulee regression6. Validate the model

model parameters

-

Some model parameters are tuned from the data (some aren’t).

- linear model coefficients are optimized (not tuned)

- k-nn value of “k” is tuned

If the model is tuned using the data, the same data cannot be used to assess the model.

With Cross Validation, you iteratively put data in your pocket.

For example, keep 1/5 of the data in your pocket, build the model on the remaining 4/5 of the data.

Cross validation for tuning parameters. Note that all of the cross validation is done on the training data.

Figure 1.8: Image credit: Alison Hill

\[\bigg\Downarrow\]

Figure 1.9: Image credit: Alison Hill

\[\bigg\Downarrow\]

Figure 8.1: Image credit: Alison Hill

\[\bigg\Downarrow\]

Figure 8.2: Image credit: Alison Hill

\[\bigg\Downarrow\]

Figure 8.3: Image credit: Alison Hill

\[\bigg\Downarrow\]

Figure 8.4: Image credit: Alison Hill

\[\bigg\Downarrow\]

Figure 8.5: Image credit: Alison Hill

\[\bigg\Downarrow\]

Figure 8.6: Image credit: Alison Hill

\[\bigg\Downarrow\]

Figure 8.7: Image credit: Alison Hill

\[\bigg\Downarrow\]

Figure 8.8: Image credit: Alison Hill

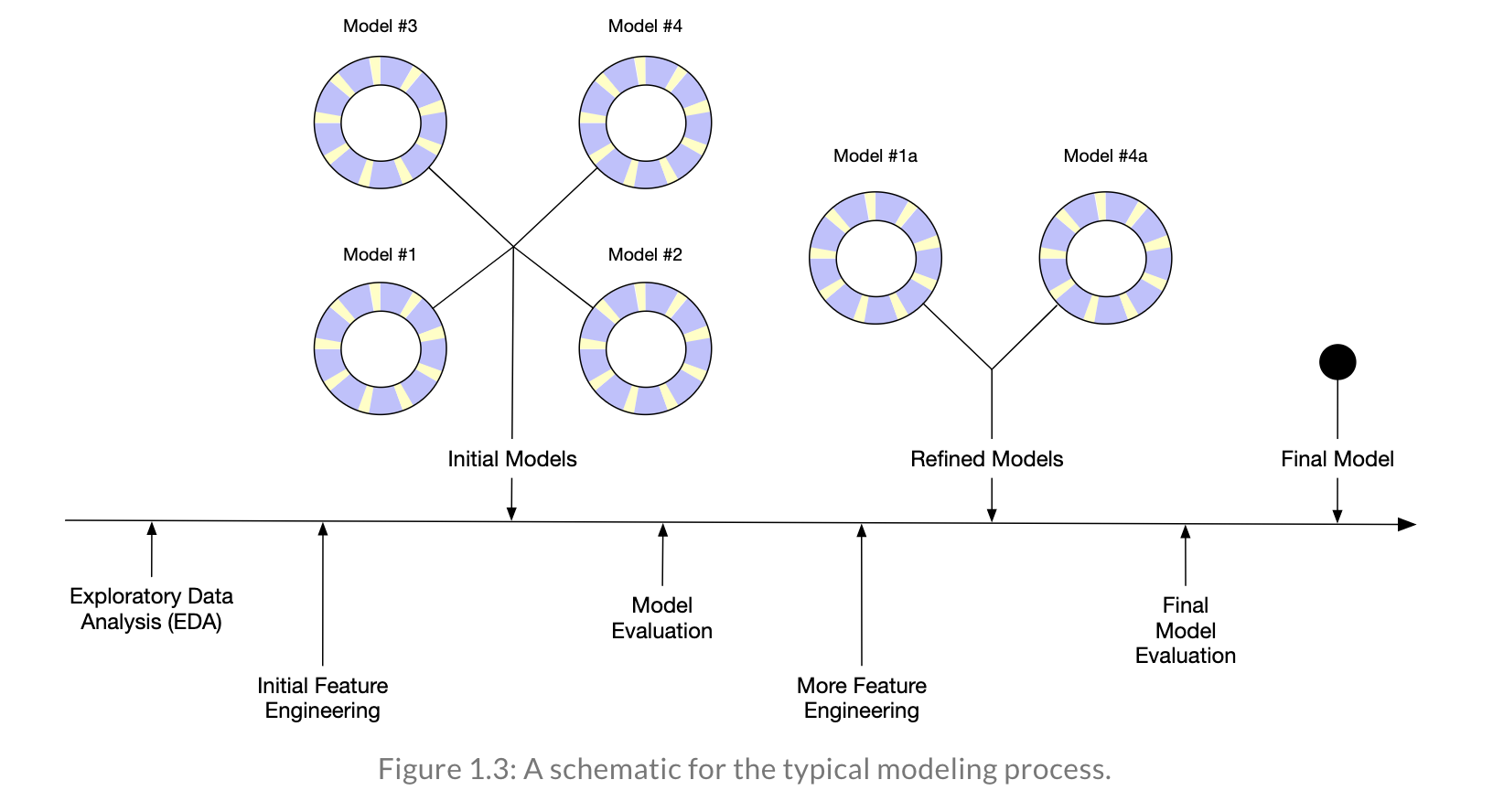

Reflecting on Model Building

In Tidy Modeling with R, Kuhn and Silge walk through an example of an entire model building process. Note that each of the stages is visited often before coming up with an appropriate model.

Figure 8.9: Image credit: https://www.tmwr.org/

Figure 8.10: Image credit: https://www.tmwr.org/

Figure 8.11: Image credit: https://www.tmwr.org/

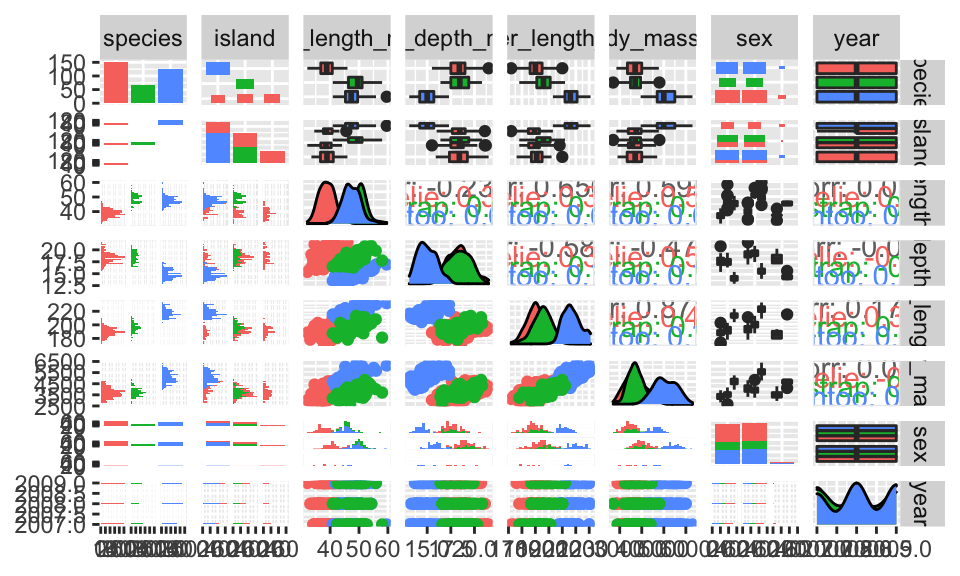

8.1.3 R model: penguins

Figure 8.12: Image credit: Alison Hill

penguins## # A tibble: 344 × 8

## species island bill_length_mm bill_depth_mm flipper_…¹ body_…² sex year

## <fct> <fct> <dbl> <dbl> <int> <int> <fct> <int>

## 1 Adelie Torgersen 39.1 18.7 181 3750 male 2007

## 2 Adelie Torgersen 39.5 17.4 186 3800 fema… 2007

## 3 Adelie Torgersen 40.3 18 195 3250 fema… 2007

## 4 Adelie Torgersen NA NA NA NA <NA> 2007

## 5 Adelie Torgersen 36.7 19.3 193 3450 fema… 2007

## 6 Adelie Torgersen 39.3 20.6 190 3650 male 2007

## 7 Adelie Torgersen 38.9 17.8 181 3625 fema… 2007

## 8 Adelie Torgersen 39.2 19.6 195 4675 male 2007

## 9 Adelie Torgersen 34.1 18.1 193 3475 <NA> 2007

## 10 Adelie Torgersen 42 20.2 190 4250 <NA> 2007

## # … with 334 more rows, and abbreviated variable names ¹flipper_length_mm,

## # ²body_mass_g

## # ℹ Use `print(n = ...)` to see more rows1. Partition the data

library(tidymodels)

library(palmerpenguins)

set.seed(47)

penguin_split <- initial_split(penguins)

penguin_train <- training(penguin_split)

penguin_test <- testing(penguin_split)2. build a recipe

penguin_recipe <-

recipe(body_mass_g ~ species + island + bill_length_mm +

bill_depth_mm + flipper_length_mm + sex + year,

data = penguin_train) %>%

step_mutate(year = as.factor(year)) %>%

step_unknown(sex, new_level = "unknown") %>%

step_relevel(sex, ref_level = "female") %>%

update_role(island, new_role = "id variable")

summary(penguin_recipe)## # A tibble: 8 × 4

## variable type role source

## <chr> <chr> <chr> <chr>

## 1 species nominal predictor original

## 2 island nominal id variable original

## 3 bill_length_mm numeric predictor original

## 4 bill_depth_mm numeric predictor original

## 5 flipper_length_mm numeric predictor original

## 6 sex nominal predictor original

## 7 year numeric predictor original

## 8 body_mass_g numeric outcome original3. select a model

penguin_lm <- linear_reg() %>%

set_engine("lm")

penguin_lm## Linear Regression Model Specification (regression)

##

## Computational engine: lm4. Create a workflow

penguin_wflow## ══ Workflow ════════════════════════════════════════════════════════════════════

## Preprocessor: Recipe

## Model: linear_reg()

##

## ── Preprocessor ────────────────────────────────────────────────────────────────

## 3 Recipe Steps

##

## • step_mutate()

## • step_unknown()

## • step_relevel()

##

## ── Model ───────────────────────────────────────────────────────────────────────

## Linear Regression Model Specification (regression)

##

## Computational engine: lm5. Fit the model

penguin_fit <- penguin_wflow %>%

fit(data = penguin_train)## # A tibble: 10 × 5

## term estimate std.error statistic p.value

## <chr> <dbl> <dbl> <dbl> <dbl>

## 1 (Intercept) -2417. 665. -3.64 3.36e- 4

## 2 speciesChinstrap -208. 92.9 -2.24 2.58e- 2

## 3 speciesGentoo 985. 152. 6.48 5.02e-10

## 4 bill_length_mm 13.5 8.29 1.63 1.04e- 1

## 5 bill_depth_mm 80.9 22.1 3.66 3.10e- 4

## 6 flipper_length_mm 20.8 3.62 5.74 2.81e- 8

## 7 sexmale 351. 52.6 6.67 1.72e-10

## 8 sexunknown 47.6 103. 0.460 6.46e- 1

## 9 year2008 -24.8 47.5 -0.521 6.03e- 1

## 10 year2009 -61.9 46.0 -1.35 1.80e- 16. Cross validation

(See Section 8.1.1 and future R examples for a full description of cross validation.)

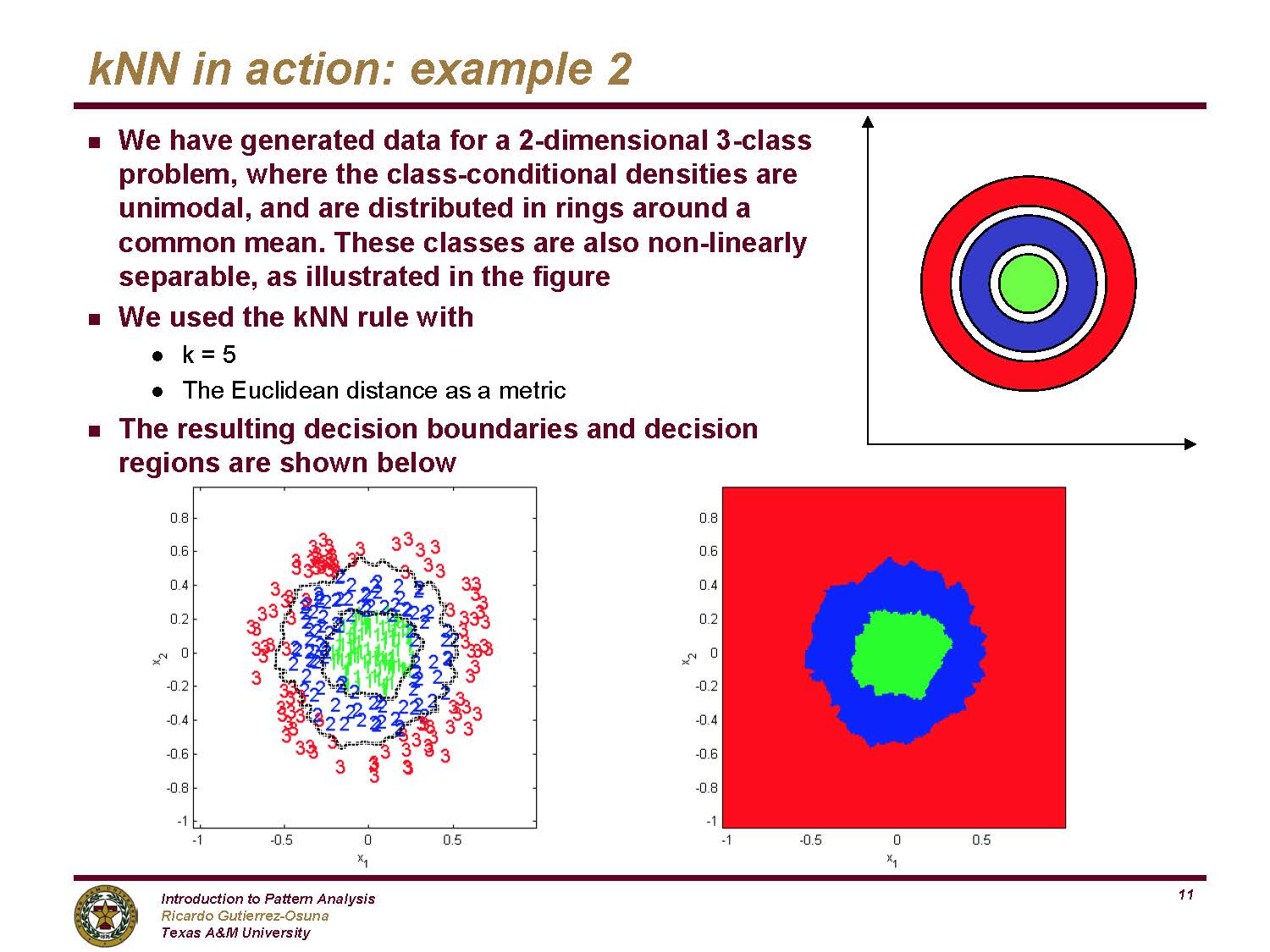

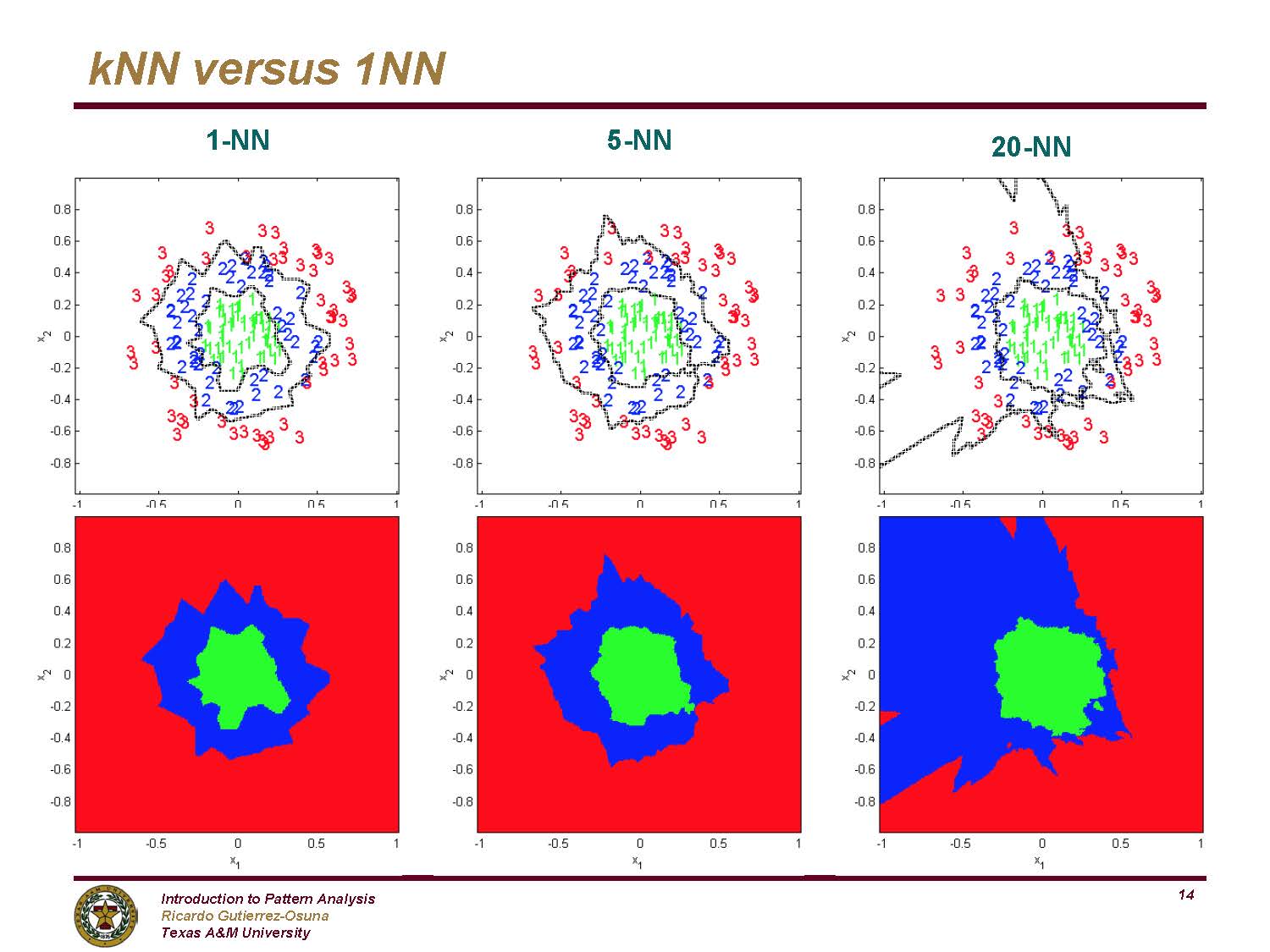

8.2 \(k\)-Nearest Neighbors

The \(k\)-Nearest Neighbor algorithm does exactly what it sounds like it does.

user decides on the integer value for \(k\)

user decides on a distance metric (most \(k\)-NN algorithms default to Euclidean distance)

a point is classified to be in the same group as the majority of the \(k\) closest points in the training data.

8.2.1 \(k\)-NN algorithm

- Decide on a distance metric (e.g., Euclidean distance, 1 - correlation, etc.) and find the distances from each point in the test set to each point in the training set. The distance is measured in the feature space, that is, with respect to the explanatory variables (not the response variable).

n.b. In most machine learning algorithms that use “distance” as a measure, the “distance” is not required to be a mathematical distance metric. Indeed, 1-correlation is a very common distance measure, and it fails the triangle inequality.

Consider a point in the test set. Find the \(k\) closest points in the training set to the one test observation.

Using majority vote, find the dominate class of the \(k\) closest points. Predict that class label to the test observation.

Note: if the response variable is continuous (instead of categorical), find the average response variable of the \(k\) training point to be the predicted response for the one test observation.

Shortcomings of \(k\)-NN:

- one class can dominate if it has a large majority

- Euclidean distance is dominated by scale

- it can be computationally unwieldy (and unneeded!!) to calculate all distances (there are algorithms to search smartly)

- the output doesn’t provide any information about which explanatory variables are informative.

- doesn’t work well with large datasets (the cost of prediction is high, and the model doesn’t always find the structure)

- doesn’t work well in high dimensions (curse of dimensionality – distance becomes meaningless in high dimensions)

- we need a lot of feature scaling

- sensitive to noise and outliers

Strengths of \(k\)-NN:

- it can easily work for any number of categories (of the outcome variable)

- it can predict a quantitative response variable

- the bias of 1-NN is often low (but the variance is high)

- any distance metric can be used (so the algorithm models the data appropriately)

- the method is straightforward to implement / understand

- there is no training period (i.e., no discrimination function is created)

- model is nonparametric (no distributional assumptions on the data)

- great model for imputing missing data

8.2.2 R k-NN: penguins

We will fit a \(k\)-Nearest Neighbor algorithm to the penguins dataset. As previously (and as to come), we’ll use the entire tidymodels workflow including partitioning the data, build a recipe, select a model, create a workflow, fit a model, and validate the model

library(GGally) # for plotting

library(tidymodels)

data(penguins)

2. Build a recipe

penguin_knn_recipe <-

recipe(species ~ body_mass_g + island + bill_length_mm +

bill_depth_mm + flipper_length_mm,

data = penguin_train) %>%

update_role(island, new_role = "id variable") %>%

step_normalize(all_predictors())

summary(penguin_knn_recipe)## # A tibble: 6 × 4

## variable type role source

## <chr> <chr> <chr> <chr>

## 1 body_mass_g numeric predictor original

## 2 island nominal id variable original

## 3 bill_length_mm numeric predictor original

## 4 bill_depth_mm numeric predictor original

## 5 flipper_length_mm numeric predictor original

## 6 species nominal outcome original3. Select a model

(note that we’ve used the default number of neighbors (here \(k=7\)).)

## K-Nearest Neighbor Model Specification (classification)

##

## Computational engine: kknn4. Create a workflow

penguin_knn_wflow <- workflow() %>%

add_model(penguin_knn) %>%

add_recipe(penguin_knn_recipe)

penguin_knn_wflow## ══ Workflow ════════════════════════════════════════════════════════════════════

## Preprocessor: Recipe

## Model: nearest_neighbor()

##

## ── Preprocessor ────────────────────────────────────────────────────────────────

## 1 Recipe Step

##

## • step_normalize()

##

## ── Model ───────────────────────────────────────────────────────────────────────

## K-Nearest Neighbor Model Specification (classification)

##

## Computational engine: kknn5. Fit (/ predict)

penguin_knn_fit <- penguin_knn_wflow %>%

fit(data = penguin_train)For the next R code chunk break it down into pieces – that is, run each line one at a time.

penguin_knn_fit %>%

predict(new_data = penguin_test) %>%

cbind(penguin_test) %>%

metrics(truth = species, estimate = .pred_class) %>%

filter(.metric == "accuracy")## # A tibble: 1 × 3

## .metric .estimator .estimate

## <chr> <chr> <dbl>

## 1 accuracy multiclass 0.988What is \(k\)?

It turns out that the default value for \(k\) in the kknn engine is 7. Is 7 best?

Cross Validation!!!

The red observations are used to fit the model, the black observations are used to assess the model.

Figure 8.13: Image credit: Alison Hill

As we saw above, cross validation randomly splits the training data into V distinct blocks of roughly equal size.

- leave out the first block of analysis data and fit a model.

- the model is used to predict the held-out block of assessment data.

- continue the process until all V assessment blocks have been predicted

The final performance is based on the hold-out predictions by averaging the statistics from the V blocks.

1b. A new partition of the training data

set.seed(470)

penguin_vfold <- vfold_cv(penguin_train,

v = 3, strata = species)3. Select a model

Now the knn model uses tune() to indicate that we actually don’t know how many neighbors to use.

5. Fit the model

The model is fit to all three of the folds created above for each value of \(k\) in k_grid.

k_grid <- data.frame(neighbors = seq(1, 15, by = 4))

k_grid## neighbors

## 1 1

## 2 5

## 3 9

## 4 13

penguin_knn_wflow_tune %>%

tune_grid(resamples = penguin_vfold,

grid = k_grid) %>%

collect_metrics() %>%

filter(.metric == "accuracy")## # A tibble: 4 × 7

## neighbors .metric .estimator mean n std_err .config

## <dbl> <chr> <chr> <dbl> <int> <dbl> <chr>

## 1 1 accuracy multiclass 0.971 2 0.00595 Preprocessor1_Model1

## 2 5 accuracy multiclass 0.977 2 0.000134 Preprocessor1_Model2

## 3 9 accuracy multiclass 0.988 2 0.0000668 Preprocessor1_Model3

## 4 13 accuracy multiclass 0.983 2 0.00568 Preprocessor1_Model46. Validate the model

Using \(k\) = 9, the model is re-trained on the training data and tested on the test data (to estimate overall model accuracy).

3. select a model

penguin_knn_final <- nearest_neighbor(neighbors = 9) %>%

set_engine("kknn") %>%

set_mode("classification")

penguin_knn_final## K-Nearest Neighbor Model Specification (classification)

##

## Main Arguments:

## neighbors = 9

##

## Computational engine: kknn4. create a workflow

penguin_knn_wflow_final <- workflow() %>%

add_model(penguin_knn_final) %>%

add_recipe(penguin_knn_recipe)

penguin_knn_wflow_final## ══ Workflow ════════════════════════════════════════════════════════════════════

## Preprocessor: Recipe

## Model: nearest_neighbor()

##

## ── Preprocessor ────────────────────────────────────────────────────────────────

## 1 Recipe Step

##

## • step_normalize()

##

## ── Model ───────────────────────────────────────────────────────────────────────

## K-Nearest Neighbor Model Specification (classification)

##

## Main Arguments:

## neighbors = 9

##

## Computational engine: kknn5. fit the model

penguin_knn_fit_final <- penguin_knn_wflow_final %>%

fit(data = penguin_train)6. validate the model

penguin_knn_fit_final %>%

predict(new_data = penguin_test) %>%

cbind(penguin_test) %>%

metrics(truth = species, estimate = .pred_class) %>%

filter(.metric == "accuracy")## # A tibble: 1 × 3

## .metric .estimator .estimate

## <chr> <chr> <dbl>

## 1 accuracy multiclass 0.977Huh. Seems like \(k=9\) didn’t do as well as \(k=7\) (the value we tried at the very beginning before cross validating).

Well, it turns out, that’s the nature of variability, randomness, and model building.

We don’t know truth, and we won’t every find a perfect model.

8.3 Decision Trees

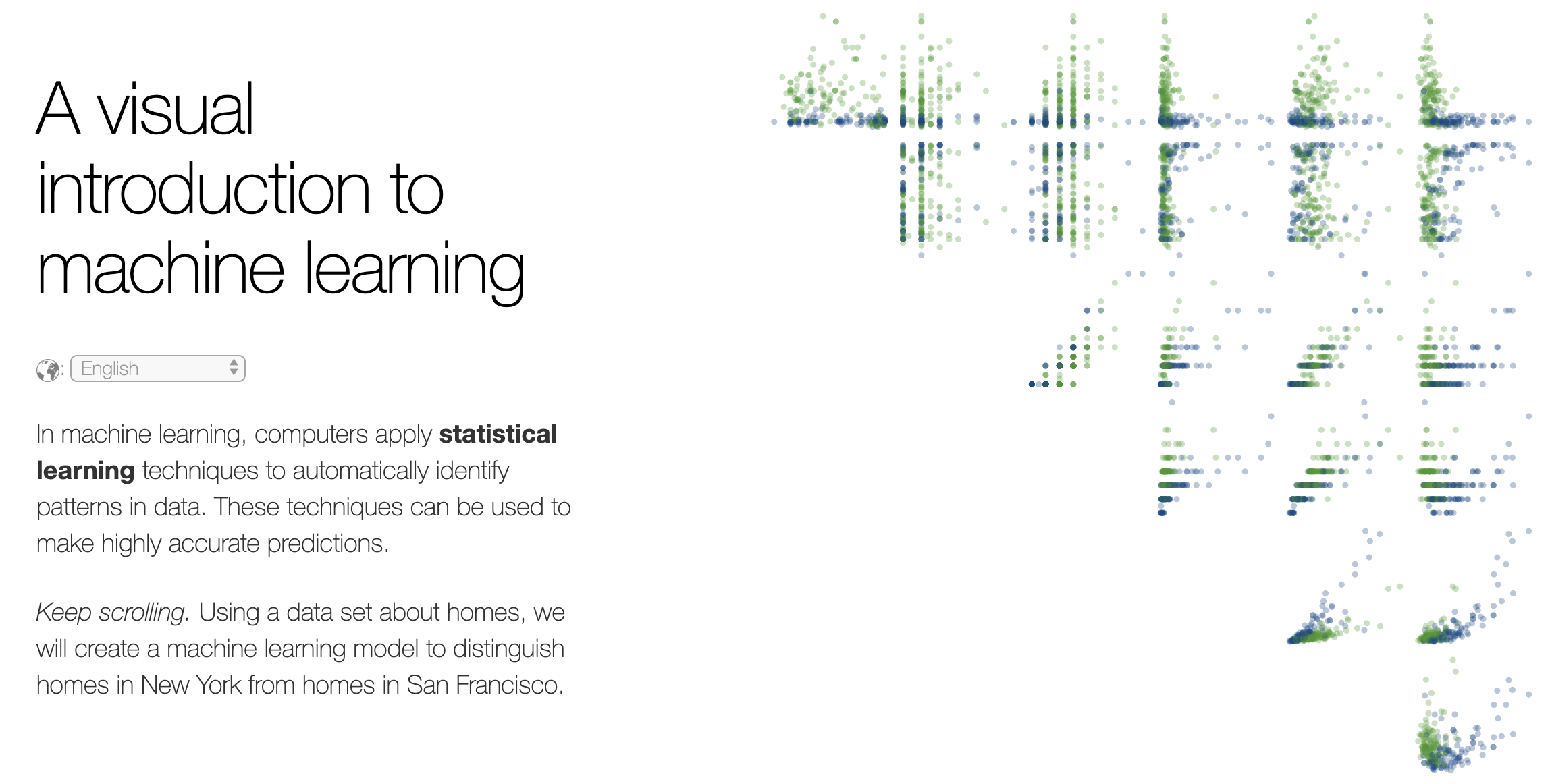

Stephanie Yee and Tony Chu created the following (amazing!) demonstration for tree intuition. Step-by-step, they build a recursive binary tree in order to model the differences between homes in SF and homes in NYC.

Figure 4.1: http://www.r2d3.us/visual-intro-to-machine-learning-part-1/ A visual introduction to machine learning.

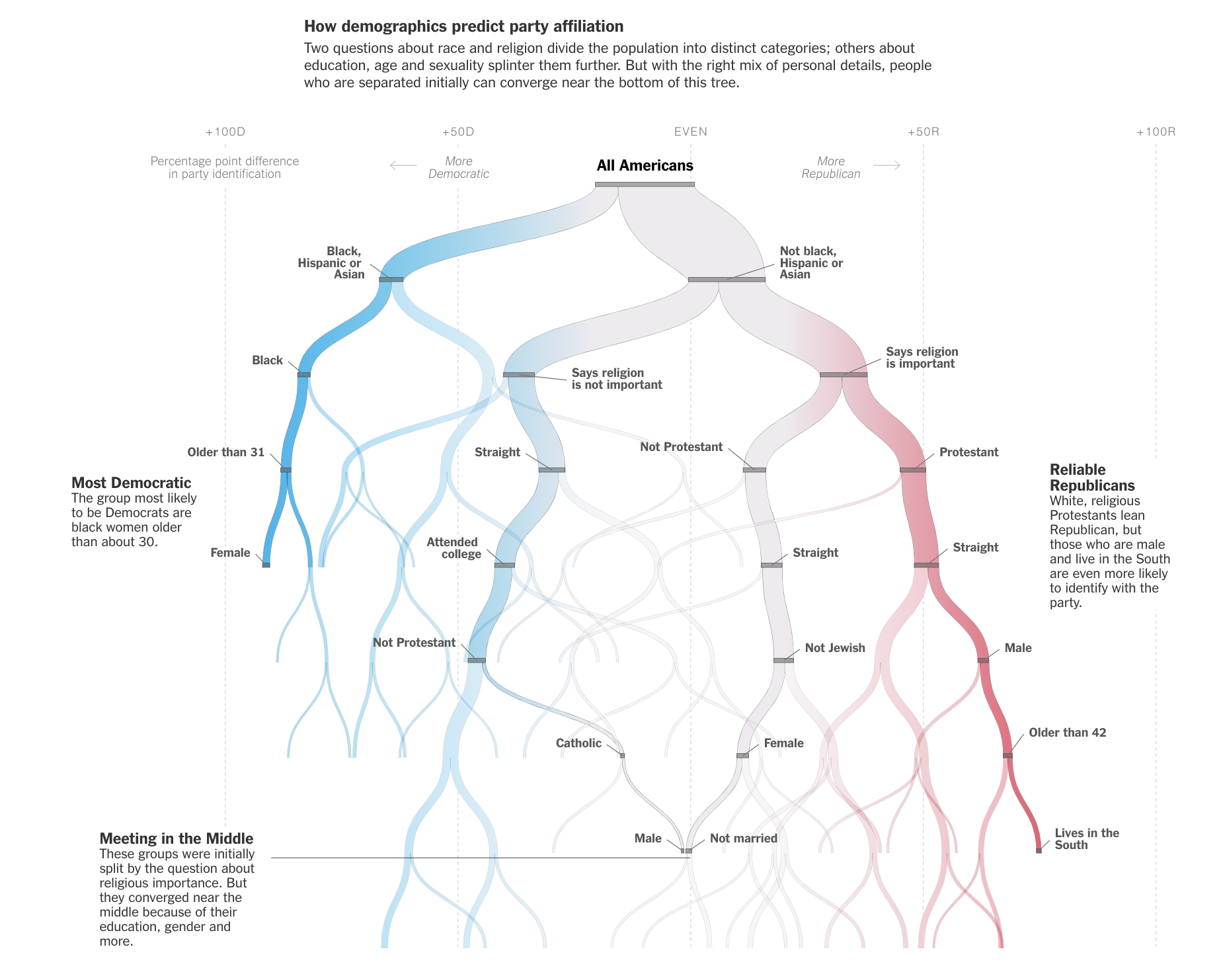

Decision trees are used for all sorts of predictive and descriptive models. The NYT created a recursive binary decision tree to show patterns in identity and political affiliation.

Figure 8.14: https://www.nytimes.com/interactive/2019/08/08/opinion/sunday/party-polarization-quiz.html Quiz: Let Us Predict Whether You’re a Democrat or a Republican NYT, Aug 8, 2019. Note that race is the first and dominant node, followed by religion.

8.3.1 CART algorithm

Basic Classification and Regression Trees (CART) Algorithm:

- Start with all observations in one group.

- Find the variable/split that best separates the response variable (successive binary partitions based on the different predictors / explanatory variables).

- Evaluation “homogeneity” within each group

- Divide the data into two groups (“leaves”) on that split (“node”).

- Within each split, find the best variable/split that separates the outcomes.

- Continue until the groups are too small or sufficiently “pure”.

- Prune tree.

Shortcomings of CART:

- Straight CART do not generally have the same predictive accuracy as other classification approaches. (we will improve the model - see Random Forests, boosting, bagging)

- Difficult to write down / consider the CART “model”

- Without proper pruning, the model can easily lead to overfitting

- With lots of predictors, (even greedy) partitioning can become computationally unwieldy

- Often, prediction performance is poor

Strengths of CART:

- They are easy to explain; trees are easy to display graphically (which make them easy to interpret). (They mirror the typical human decision-making process.)

- Can handle categorical or numerical predictors or response variables (indeed, they can handle mixed predictors at the same time!).

- Can handle more than 2 groups for categorical predictions

- Easily ignore redundant variables.

- Perform better than linear models in non-linear settings. Classification trees are non-linear models, so they immediately use interactions between variables.

- Data transformations may be less important (monotone transformations on the explanatory variables won’t change anything).

Classification Trees

A classification tree is used to predict a categorical response variable (rather than a quantitative one). The end predicted value will be the one of the most commonly occurring class of training observations in the region to which it belongs. The goal is to create regions which are as homogeneous as possible with respect to the response variable - categories.

measures of impurity

- Calculate the classification error rate as the fraction of the training observations in that region that do not belong to the most common class: \[E_m = 1 - \max_k(\hat{p}_{mk})\] where \(\hat{p}_{mk}\) represents the proportion of training observations in the \(m\)th region that are from the \(k\)th class. However, the classification error rate is not particularly sensitive to node purity, and so two additional measures are typically used to partition the regions.

- Further, the Gini index is defined by \[G_m= \sum_{k=1}^K \hat{p}_{mk}(1-\hat{p}_{mk})\] a measure of total variance across the \(K\) classes. [Recall, the variance of a Bernoulli random variable with \(\pi\) = P(success) is \(\pi(1-\pi)\).] Note that the Gini index takes on a small value if all of the \(\hat{p}_{mk}\) values are close to zero or one. For this reason, the Gini index is referred to as a measure of node purity - a small value indicates that a node contains predominantly observations from a single class.

- Last, the cross-entropy is defined as \[D_m = - \sum_{k=1}^K \hat{p}_{mk} \log \hat{p}_{mk}\] Since \(0 \leq \hat{p}_{mk} \leq 1\) it follows that \(0 \leq -\hat{p}_{mk} \log\hat{p}_{mk}\). One can show that the cross-entropy will take on a value near zero if the \(\hat{p}_{mk}\) values are all near zero or all near one. Therefore, like the Gini index, the cross-entropy will take on a small value if the \(m\)th node is pure.

- To build the tree, typically the Gini index or the cross-entropy are used to evaluate a particular split.

- To prune the tree, often classification error is used (if accuracy of the final pruned tree is the goal)

Computationally, it is usually infeasible to consider every possible partition of the observations. Instead of looking at all partitions, we perform a top down approach to the problem which is known as recursive binary splitting (greedy because we look only at the current split and not at the outcomes of the splits to come).

Recursive Binary Splitting on Categories (for a given node)

- Select the predictor \(X_j\) and the cutpoint \(s\) such that splitting the predictor space into the regions \(\{X | X_j< s\}\) and \(\{X | X_j \geq s\}\) lead to the greatest reduction in Gini index or cross-entropy.

- For any \(j\) and \(s\), define the pair of half-planes to be \[R_1(j,s) = \{X | X_j < s\} \mbox{ and } R_2(j,s) = \{X | X_j \geq s\}\] and we seek the value of \(j\) and \(s\) that minimize the equation: \[\begin{align} & \sum_{i:x_i \in R_1(j,s)} \sum_{k=1}^K \hat{p}_{{R_1}k}(1-\hat{p}_{{R_1}k}) + \sum_{i:x_i \in R_2(j,s)} \sum_{k=1}^K \hat{p}_{{R_2}k}(1-\hat{p}_{{R_2}k})\\ \mbox{equivalently: } & n_{R_1} \sum_{k=1}^K \hat{p}_{{R_1}k}(1-\hat{p}_{{R_1}k}) + n_{R_2} \sum_{k=1}^K \hat{p}_{{R_2}k}(1-\hat{p}_{{R_2}k})\\ \end{align}\]

- Repeat the process, looking for the best predictor and best cutpoint within one of the previously identified regions (producing three regions, now).

- Keep repeating the process until a stopping criterion is reached - for example, until no region contains more than 5 observations.

Regression Trees

The goal of the algorithm in a regression tree is to split the set of possible value for the data into \(|T|\) distinct and non-overlapping regions, \(R_1, R_2, \ldots, R_{|T|}\). For every observation that falls into the region \(R_m\), we make the same prediction - the mean of the response values for the training observations in \(R_m\). So how do we find the regions \(R_1, \ldots, R_{|T|}\)?

\(\Rightarrow\) Minimize RSS, \[RSS = \sum_{m=1}^{|T|} \sum_{i \in R_m} (y_i - \overline{y}_{R_m})^2\] where \(\overline{y}_{R_m}\) is the mean response for the training observations within the \(m\)th region.

(Note: in the chapter (James et al. 2021) they refer to MSE - mean squared error - in addition to RSS where MSE is simply RSS / n, see equation (2.5).)

Again, it is usually infeasible to consider every possible partition of the observations. Instead of looking at all partitions, we perform a top down approach to the problem which is known as recursive binary splitting (greedy because we look only at the current split and not at the outcomes of the splits to come).

Recursive Binary Splitting on Numerical Response (for a given node)

- Select the predictor \(X_j\) and the cutpoint \(s\) such that splitting the predictor space into the regions \(\{X | X_j< s\}\) and \(\{X | X_j \geq s\}\) lead to the greatest reduction in RSS.

- For any \(j\) and \(s\), define the pair of half-planes to be \[R_1(j,s) = \{X | X_j < s\} \mbox{ and } R_2(j,s) = \{X | X_j \geq s\}\] and we see the value of \(j\) and \(s\) that minimize the equation: \[\sum_{i:x_i \in R_1(j,s)} (y_i - \overline{y}_{R_1})^2 + \sum_{i:x_i \in R_2(j,s)} (y_i - \overline{y}_{R_2})^2\] where \(\overline{y}_{R_1}\) is the mean response for the training observations in \(R_1(j,s)\) and \(\overline{y}_{R_2}\) is the mean response for training observations in \(R_2(j,s)\).

- Repeat the process, looking for the best predictor and best cutpoint within one of the previously identified regions (producing three regions, now).

- Keep repeating the process until a stopping criterion is reached - for example, until no region contains more than 5 observations.

(Avoiding) Overfitting

Ideally, the tree would not overfit the training data. One could imagine how easy it would be to grow the tree over the training data so as to end up with terminal nodes which are completely homogeneous (but then don’t represent the test data).

See the following (amazing!) demonstration for intuition on model validation / overfitting: http://www.r2d3.us/visual-intro-to-machine-learning-part-2/

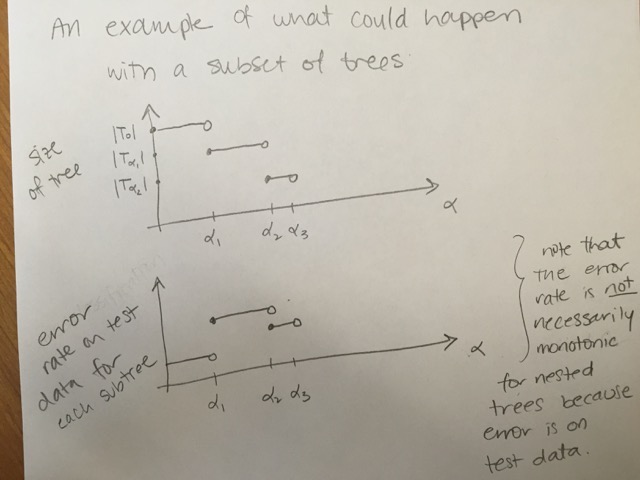

One possible algorithm for building a tree is to split based on the reduction in RSS (or Gini index, etc.) exceeding some (presumably high) threshold. However, the strategy is known to be short sighted, as a split later down the tree may contain a large amount of information. A better strategy is to grow a very large tree \(T_0\) and then prune it back in order to obtain a subtree. Use cross validation to build the subtree so as to not overfit the data.

Algorithm: Building a Regression Tree

- Use recursive binary splitting to grow a large tree on the training data, stopping only when each terminal node has fewer than some minimum number of observations.

- Apply cost complexity pruning to the large tree in order to obtain a sequence of best subtrees, as a function of \(\alpha\).

- Use \(V\)-fold cross-validation to choose \(\alpha\). That is, divide the training observations into \(V\) folds. For each \(v=1, 2, \ldots, V\):

- Repeat Steps 1 and 2 on all but the \(V\)th fold of the training data.

- Evaluate the mean squared prediction error on the data in the left-out \(k\)th fold, as a function of \(\alpha\). For each value of \(\alpha\), average the prediction error (either misclassification or RSS), and pick \(\alpha\) to minimize the average error.

- Return the subtree from Step 2 that corresponds to the chosen value of \(\alpha\).

Cost Complexity Pruning

Also known as weakest link pruning, the idea is to consider a sequence of trees indexed by a nonnegative tuning parameter \(\alpha\) (instead of considering every single subtree). Generally, the idea is that there is a cost to having a larger (more complex!) tree. We define the cost complexity criterion (\(\alpha > 0\)): \[\begin{align} \mbox{numerical: } C_\alpha(T) &= \sum_{m=1}^{|T|} \sum_{i \in R_m} (y_i - \overline{y}_{R_m})^2 + \alpha \cdot |T|\\ \mbox{categorical: } C_\alpha(T) &= \sum_{m=1}^{|T|} \sum_{i \in R_m} I(y_i \ne k(m)) + \alpha \cdot |T| \end{align}\] where \(k(m)\) is the class with the majority of observations in node \(m\) and \(|T|\) is the number of terminal nodes in the tree.

- \(\alpha\) small: If \(\alpha\) is set to be small, we are saying that the risk is more worrisome than the complexity and larger trees are favored because they reduce the risk.

- \(\alpha\) large: If \(\alpha\) is set to be large, then the complexity of the tree is more worrisome and smaller trees are favored.

The way to think about cost complexity is to consider \(\alpha\) increasing. As \(\alpha\) gets bigger, the “best” tree will be smaller. But the test error will not be monotonically related to the size of the training tree.

A note on \(\alpha\)

In the text (Introduction to Statistical Learning) and almost everywhere else you might look, the cost complexity is defined as in previous slides.

However, you might notice that in R the cost_complexity value is typically less than 1. From what I can tell, the value of the function that is being minimized in R is the average of the squared errors and the missclassification rate.

\[\begin{align} \mbox{numerical: } C_\alpha(T) &= \frac{1}{n}\sum_{m=1}^{|T|} \sum_{i \in R_m} (y_i - \overline{y}_{R_m})^2 + \alpha \cdot |T|\\ \mbox{categorical: } C_\alpha(T) &= \frac{1}{n}\sum_{m=1}^{|T|} \sum_{i \in R_m} I(y_i \ne k(m)) + \alpha \cdot |T| \end{align}\]

Variations on a theme

The main ideas above are consistent throughout all CART algorithms. However, the exact details of implementation can change from function to function, and often times it is very difficult to decipher exactly which equation is being used. In the tree function in R, much of the decision making is done on deviance which is defined as:

\[\mbox{numerical: deviance} = \sum_{m=1}^{|T|} \sum_{i \in R_m} (y_i - \overline{y}_{R_m})^2\]

\[\mbox{categorical: deviance} = -2\sum_{m=1}^{|T|} \sum_{k=1}^K n_{mk} \log \hat{p}_{mk}\]

For the CART algorithm, minimize the deviance (for both types of variables). The categorical deviance will be small if most of the observations are in the majority group (with high proportion). Also, \(\lim_{\epsilon \rightarrow 0} \epsilon \log(\epsilon) = 0\). Additionally, methods of cross validation can also vary. In particular, if the number of variables is large, the tree algorithm can be slow and so the cross validation process - choice of \(\alpha\) - needs to be efficient.

CV for model building and model assessment

Notice that CV is used for both model building and model assessment. It is possible (and practical, though quite computational!) to use both practices on the same classification model. The algorithm could be as follows.

Algorithm: CV for both \(V_1\)-fold CV building and \(V_2\)-fold CV assessment

- Partition the data in \(V_1\) groups.

- Remove the first group, and train the data on the remaining \(V_1-1\) groups.

- Use \(V_2\)-fold cross-validation (on the \(V_1-1\) groups) to choose \(\alpha\). That is, divide the training observations into \(V_2\) folds and find \(\alpha\) that minimizes the error.

- Using the subtree that corresponds to the chosen value of \(\alpha\), predict the first of the \(V_1\) hold out samples.

- Repeat steps 2-4 using the remaining \(V_1 - 1\) groups.

8.3.2 R CART Example

The Census Bureau divides the country up into “tracts” of approximately equal population. For the 1990 Census, California was divided into 20640 tracts. One data sets (houses on http://lib.stat.cmu.edu/datasets/; http://lib.stat.cmu.edu/datasets/houses.zip) records the following for each tract in California: Median house price, median house age, total number of rooms, total number of bedrooms, total number of occupants, total number of houses, median income (in thousands of dollars), latitude and longitude. It appeared in Pace and Barry (1997), “Sparse Spatial Autoregressions”, Statistics and Probability Letters.

Classification and Regression Trees

Classification Trees are used to predict a response or class \(Y\) from input \(X_1, X_2, \ldots, X_n\). If it is a continuous response it’s called a regression tree, if it is categorical, it’s called a classification tree. At each node of the tree, we check the value of one the input \(X_i\) and depending of the (binary) answer we continue to the left or to the right subbranch. When we reach a leaf we will find the prediction (usually it is a simple statistic of the dataset the leaf represents, like the most common value from the available classes).

Note on maxdepth: as you might expect, maxdepth indicates the longest length from the root of the tree to a terminal node. However, for rpart (in particular, using rpart or rpart2 in caret), there are other default settings that keep the tree from growing all the way to singular nodes, even with a high maxdepth.

Regression Trees

For technical reasons (e.g., see here), the step_log() on the outcome variable step gives problems with predictions at the end. Therefore, we mutate the outcome variable within the dataset before starting the model building process.

real.estate <- read.table("http://pages.pomona.edu/~jsh04747/courses/math154/CA_housedata.txt",

header=TRUE) %>%

mutate(logValue = log(MedianHouseValue))

# partition

set.seed(47)

house_split <- initial_split(real.estate)

house_train <- training(house_split)

house_test <- testing(house_split)

# recipe

house_cart_recipe <-

recipe(logValue ~ Longitude + Latitude ,

data = house_train)

# model

house_cart <- decision_tree() %>%

set_engine("rpart") %>%

set_mode("regression")

# workflow

house_cart_wflow <- workflow() %>%

add_model(house_cart) %>%

add_recipe(house_cart_recipe)

# fit

house_cart_fit <- house_cart_wflow %>%

fit(data = house_train)Model Output

house_cart_fit## ══ Workflow [trained] ══════════════════════════════════════════════════════════

## Preprocessor: Recipe

## Model: decision_tree()

##

## ── Preprocessor ────────────────────────────────────────────────────────────────

## 0 Recipe Steps

##

## ── Model ───────────────────────────────────────────────────────────────────────

## n= 15480

##

## node), split, n, deviance, yval

## * denotes terminal node

##

## 1) root 15480 5024.405000 12.08947

## 2) Latitude>=38.485 1541 283.738200 11.59436

## 4) Latitude>=39.355 506 48.267930 11.31530 *

## 5) Latitude< 39.355 1035 176.803400 11.73079 *

## 3) Latitude< 38.485 13939 4321.152000 12.14421

## 6) Longitude>=-121.645 10454 3320.946000 12.06198

## 12) Latitude>=34.635 2166 491.986400 11.52110

## 24) Longitude>=-120.265 1083 166.051200 11.28432 *

## 25) Longitude< -120.265 1083 204.505800 11.75787 *

## 13) Latitude< 34.635 8288 2029.685000 12.20333

## 26) Longitude>=-118.315 6240 1373.830000 12.09295

## 52) Longitude>=-117.575 2130 516.313400 11.87918

## 104) Latitude>=33.605 821 123.684300 11.64002 *

## 105) Latitude< 33.605 1309 316.218800 12.02918

## 210) Longitude>=-116.33 97 8.931327 11.17127 *

## 211) Longitude< -116.33 1212 230.181300 12.09784

## 422) Longitude>=-117.165 796 101.805300 11.94935 *

## 423) Longitude< -117.165 416 77.245280 12.38196 *

## 53) Longitude< -117.575 4110 709.740000 12.20373

## 106) Latitude>=33.735 3529 542.838300 12.14908

## 212) Latitude< 34.105 2931 379.526800 12.09154

## 424) Longitude< -118.165 1114 147.375800 11.91911 *

## 425) Longitude>=-118.165 1817 178.722200 12.19726 *

## 213) Latitude>=34.105 598 106.051400 12.43109 *

## 107) Latitude< 33.735 581 92.340630 12.53568 *

## 27) Longitude< -118.315 2048 348.149000 12.53967

## 54) Latitude>=34.165 949 106.791800 12.38022 *

## 55) Latitude< 34.165 1099 196.395200 12.67735

## 110) Longitude>=-118.365 431 85.796770 12.38191 *

## 111) Longitude< -118.365 668 48.703000 12.86798 *

## 7) Longitude< -121.645 3485 717.479900 12.39087

## 14) Latitude>=37.925 796 133.300900 12.10055 *

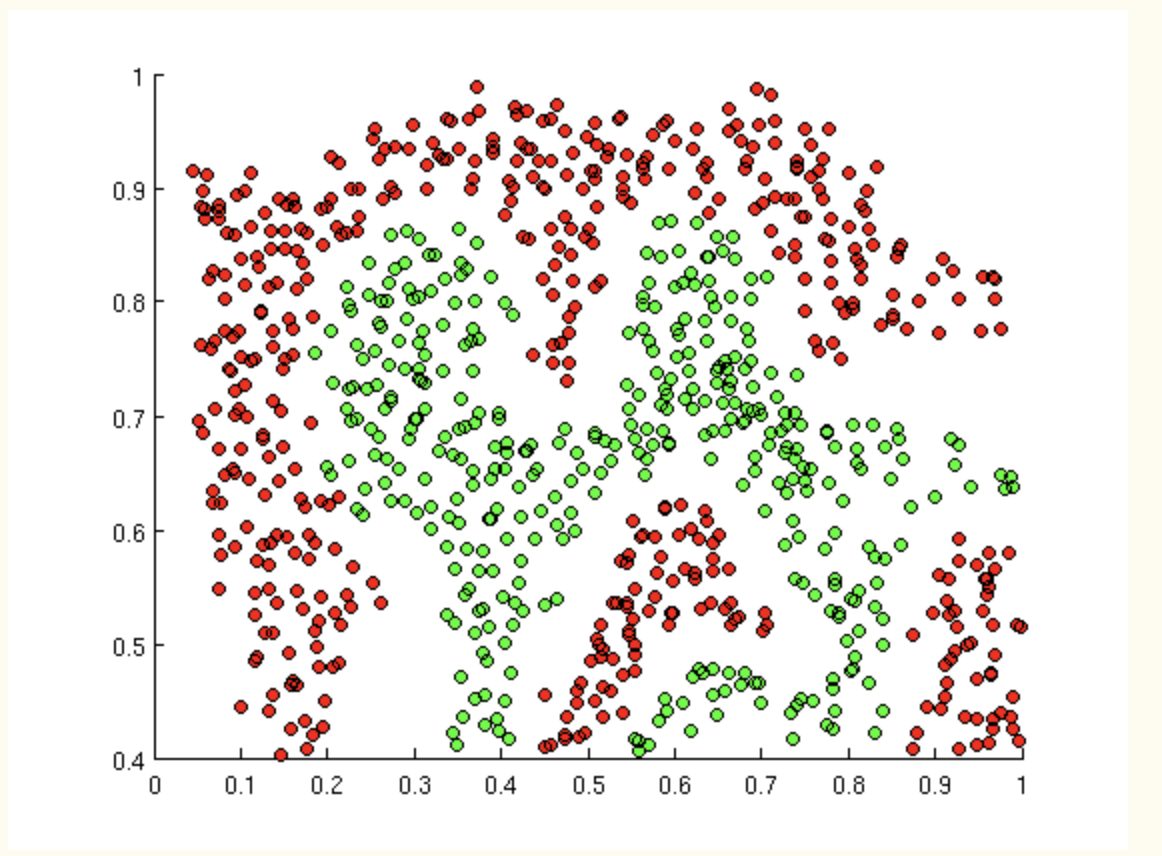

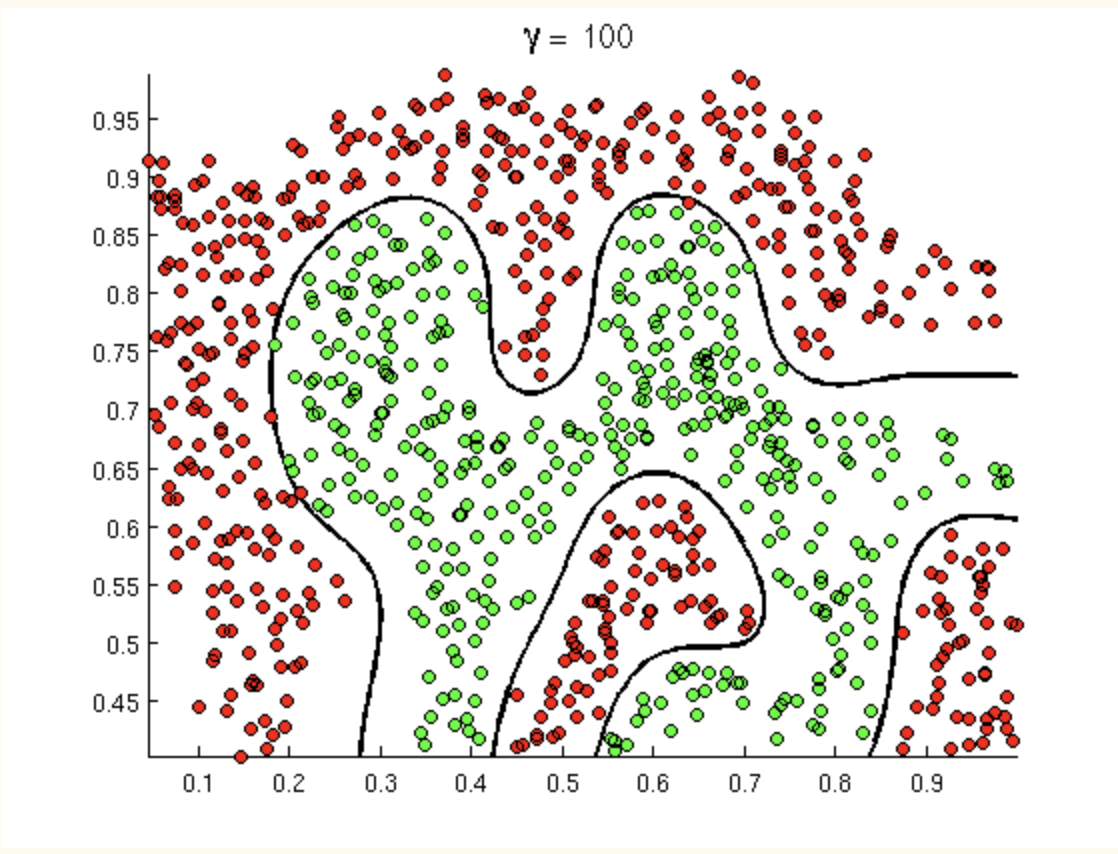

## 15) Latitude< 37.925 2689 497.226200 12.47681 *The following scatter plot can only be made when the CART is built using two numerical predictor variables.

#remotes::install_github("grantmcdermott/parttree")

library(parttree)

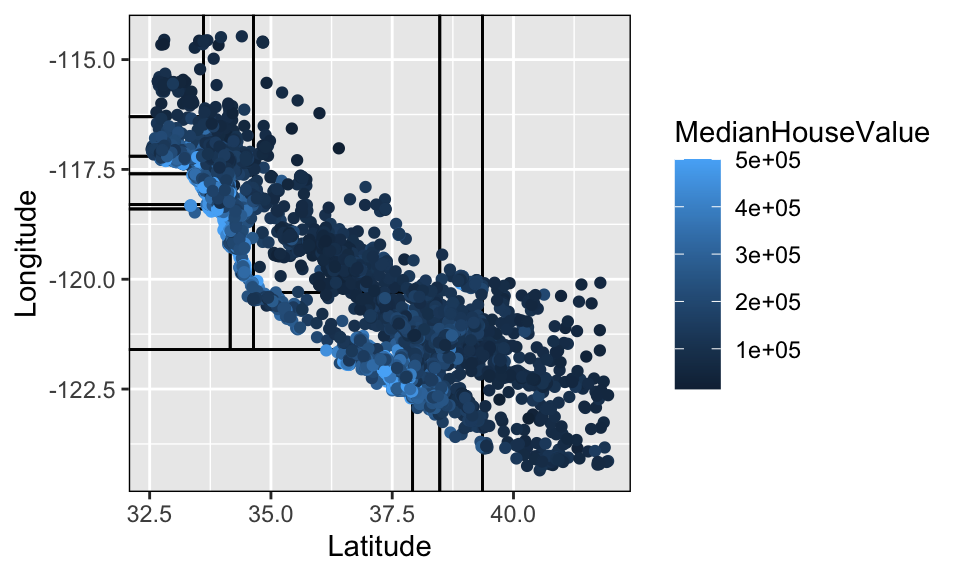

house_train %>%

ggplot(aes(y = Longitude, x = Latitude)) +

geom_parttree(data = house_cart_fit, alpha = 0.2) +

geom_point(aes(color = MedianHouseValue))

Predicting

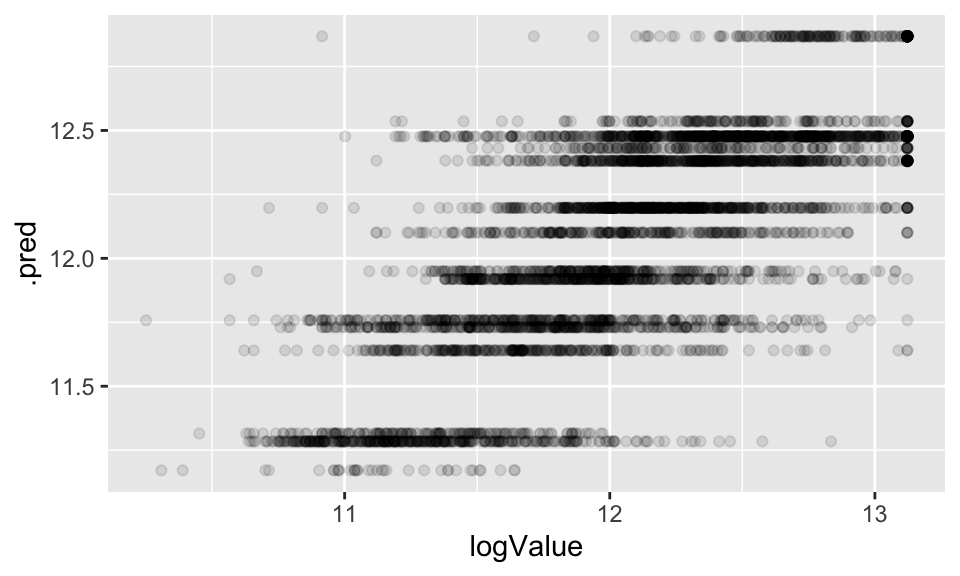

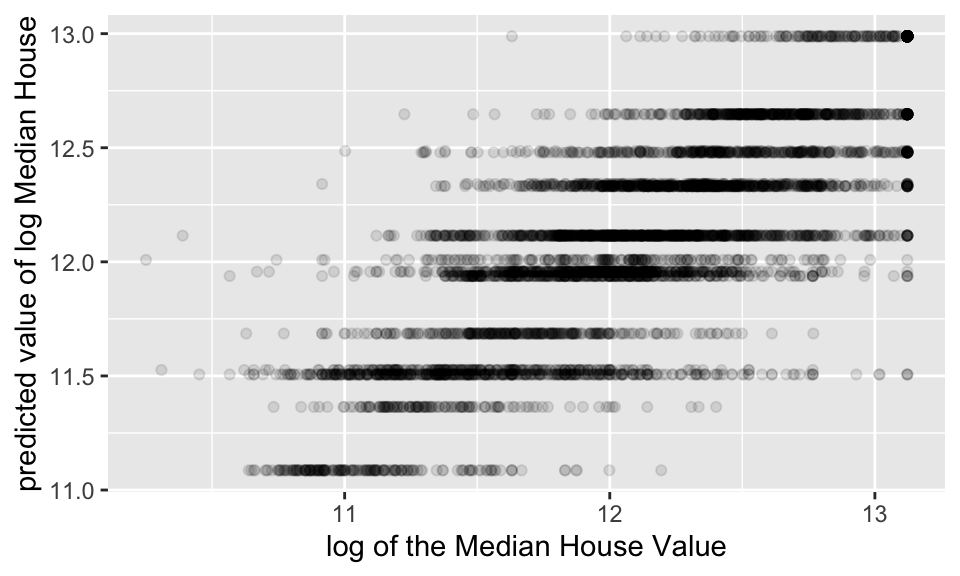

As seen in the image above, there are only 12 region so there are only 12 predicted values. The plot below seems a little odd at first glance, but it should make sense after careful consideration of what is the outcome measurement and what is the predicted value.

house_cart_fit %>%

predict(new_data = house_test) %>%

cbind(house_test) %>%

ggplot() +

geom_point(aes(x = logValue, y = .pred), alpha = 0.1)

Finer partition

From above:

12) Latitude>=34.675 2182 513.95640 11.52385 The node that splits at latitude greater than 34.675 has 2182 houses. 513.9564 is the “deviance” which is the sum of squares value for that node. The predicted value is the average of the points in that node: 11.5. It is not a terminal node (no asterisk).

More variables

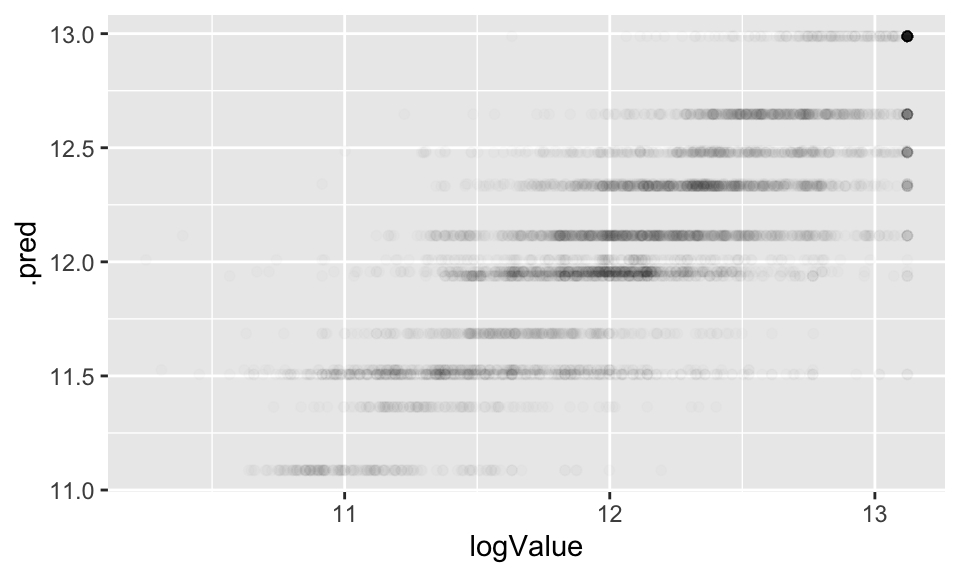

Including all the variables, not only the latitude and longitude. Note the predictions are much better!

real.estate <- read.table("http://pages.pomona.edu/~jsh04747/courses/math154/CA_housedata.txt",

header=TRUE) %>%

mutate(logValue = log(MedianHouseValue))

# partition

set.seed(47)

house_split <- initial_split(real.estate)

house_train <- training(house_split)

house_test <- testing(house_split)

# recipe

house_cart_full_recipe <-

recipe(logValue ~ . ,

data = house_train) %>%

update_role(MedianHouseValue, new_role = "id variable")

# model

house_cart <- decision_tree() %>%

set_engine("rpart") %>%

set_mode("regression")

# workflow

house_cart_full_wflow <- workflow() %>%

add_model(house_cart) %>%

add_recipe(house_cart_full_recipe)

# fit

house_cart_full_fit <- house_cart_full_wflow %>%

fit(data = house_train)

house_cart_full_fit %>%

predict(new_data = house_test) %>%

cbind(house_test) %>%

ggplot() +

geom_point(aes(x = logValue, y = .pred), alpha = 0.01)

Cross Validation (model building!)

real.estate <- read.table("http://pages.pomona.edu/~jsh04747/courses/math154/CA_housedata.txt",

header=TRUE) %>%

mutate(logValue = log(MedianHouseValue))

# partition

set.seed(47)

house_split <- initial_split(real.estate)

house_train <- training(house_split)

house_test <- testing(house_split)

set.seed(4321)

house_vfold <- vfold_cv(house_train, v = 10)

cart_grid <- expand.grid(tree_depth = seq(2, 20, by = 2))

# recipe

house_cart_tune_recipe <-

recipe(logValue ~ .,

data = house_train) %>%

update_role(MedianHouseValue, new_role = "id variable")

# model

house_cart_tune <- decision_tree(tree_depth = tune()) %>%

set_engine("rpart") %>%

set_mode("regression")

# workflow

house_cart_tune_wflow <- workflow() %>%

add_model(house_cart_tune) %>%

add_recipe(house_cart_tune_recipe)

# tuning / fit

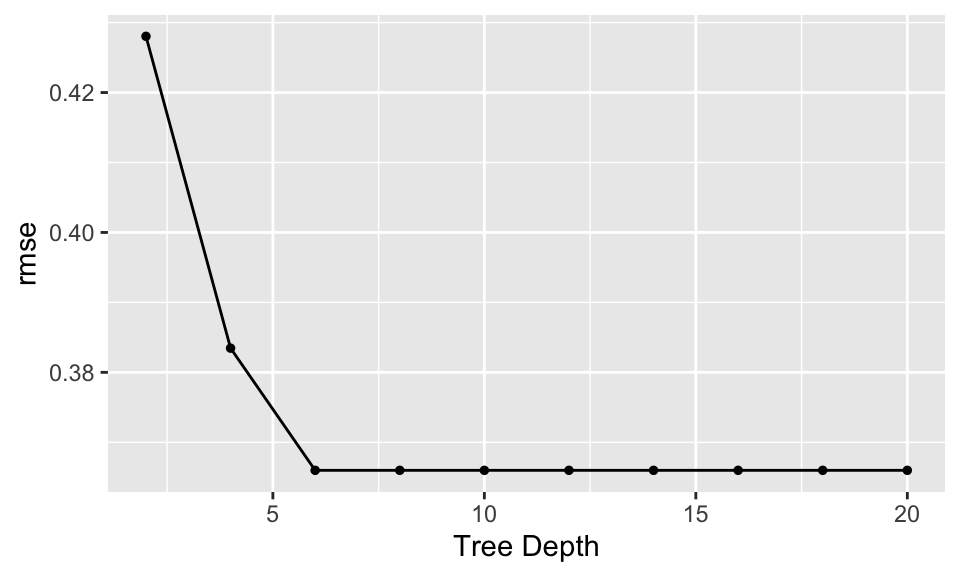

house_tuned <- house_cart_tune_wflow %>%

tune_grid(resamples = house_vfold,

grid = cart_grid) CV accuracy

## # A tibble: 20 × 7

## tree_depth .metric .estimator mean n std_err .config

## <dbl> <chr> <chr> <dbl> <int> <dbl> <chr>

## 1 2 rmse standard 0.428 10 0.00224 Preprocessor1_Model01

## 2 2 rsq standard 0.436 10 0.00665 Preprocessor1_Model01

## 3 4 rmse standard 0.383 10 0.00242 Preprocessor1_Model02

## 4 4 rsq standard 0.547 10 0.00629 Preprocessor1_Model02

## 5 6 rmse standard 0.366 10 0.00239 Preprocessor1_Model03

## 6 6 rsq standard 0.588 10 0.00586 Preprocessor1_Model03

## 7 8 rmse standard 0.366 10 0.00239 Preprocessor1_Model04

## 8 8 rsq standard 0.588 10 0.00586 Preprocessor1_Model04

## 9 10 rmse standard 0.366 10 0.00239 Preprocessor1_Model05

## 10 10 rsq standard 0.588 10 0.00586 Preprocessor1_Model05

## 11 12 rmse standard 0.366 10 0.00239 Preprocessor1_Model06

## 12 12 rsq standard 0.588 10 0.00586 Preprocessor1_Model06

## 13 14 rmse standard 0.366 10 0.00239 Preprocessor1_Model07

## 14 14 rsq standard 0.588 10 0.00586 Preprocessor1_Model07

## 15 16 rmse standard 0.366 10 0.00239 Preprocessor1_Model08

## 16 16 rsq standard 0.588 10 0.00586 Preprocessor1_Model08

## 17 18 rmse standard 0.366 10 0.00239 Preprocessor1_Model09

## 18 18 rsq standard 0.588 10 0.00586 Preprocessor1_Model09

## 19 20 rmse standard 0.366 10 0.00239 Preprocessor1_Model10

## 20 20 rsq standard 0.588 10 0.00586 Preprocessor1_Model10

house_tuned %>%

select_best("rmse")## # A tibble: 1 × 2

## tree_depth .config

## <dbl> <chr>

## 1 6 Preprocessor1_Model03Final model + prediction on test data

Turns out that the tree does “better” by being more complex – why is that? The tree with 14 nodes (depth of 6) corresponds to the tree with the lowest deviance.

# recipe

house_cart_final_recipe <-

recipe(logValue ~ .,

data = house_train) %>%

update_role(MedianHouseValue, new_role = "id variable")

# model

house_cart_final <- decision_tree(tree_depth = 6) %>%

set_engine("rpart") %>%

set_mode("regression")

# workflow

house_cart_final_wflow <- workflow() %>%

add_model(house_cart_final) %>%

add_recipe(house_cart_final_recipe)

# tuning / fit

house_final <- house_cart_final_wflow %>%

fit(data = house_train)Predicting the final model on test data

house_final## ══ Workflow [trained] ══════════════════════════════════════════════════════════

## Preprocessor: Recipe

## Model: decision_tree()

##

## ── Preprocessor ────────────────────────────────────────────────────────────────

## 0 Recipe Steps

##

## ── Model ───────────────────────────────────────────────────────────────────────

## n= 15480

##

## node), split, n, deviance, yval

## * denotes terminal node

##

## 1) root 15480 5024.40500 12.08947

## 2) MedianIncome< 3.54635 7696 1992.69800 11.77343

## 4) MedianIncome< 2.5165 3632 904.76740 11.57590

## 8) Latitude>=34.445 1897 412.81950 11.38488

## 16) Longitude>=-120.265 549 63.97662 11.08633 *

## 17) Longitude< -120.265 1348 279.98120 11.50647 *

## 9) Latitude< 34.445 1735 347.04430 11.78476

## 18) Longitude>=-117.775 645 111.86670 11.52607 *

## 19) Longitude< -117.775 1090 166.47070 11.93784 *

## 5) MedianIncome>=2.5165 4064 819.58450 11.94995

## 10) Latitude>=37.925 809 91.49688 11.68589 *

## 11) Latitude< 37.925 3255 657.65510 12.01558

## 22) Longitude>=-122.235 2992 563.13610 11.97426

## 44) Latitude>=34.455 940 203.99070 11.77685

## 88) Longitude>=-120.155 338 31.54079 11.36422 *

## 89) Longitude< -120.155 602 82.59029 12.00852 *

## 45) Latitude< 34.455 2052 305.72870 12.06470

## 90) Longitude>=-118.285 1476 171.16160 11.95681 *

## 91) Longitude< -118.285 576 73.36843 12.34115 *

## 23) Longitude< -122.235 263 31.29310 12.48567 *

## 3) MedianIncome>=3.54635 7784 1502.97400 12.40194

## 6) MedianIncome< 5.59185 5526 876.96730 12.25670

## 12) MedianHouseAge< 38.5 4497 651.27750 12.20567

## 24) MedianIncome< 4.53095 2616 388.38650 12.11491 *

## 25) MedianIncome>=4.53095 1881 211.37640 12.33189 *

## 13) MedianHouseAge>=38.5 1029 162.80030 12.47972 *

## 7) MedianIncome>=5.59185 2258 224.13060 12.75740

## 14) MedianIncome< 7.393 1527 134.00030 12.64684 *

## 15) MedianIncome>=7.393 731 32.47344 12.98835 *

house_final %>%

predict(new_data = house_test) %>%

cbind(house_test) %>%

ggplot() +

geom_point(aes(x = logValue, y = .pred), alpha = 0.1) +

xlab("log of the Median House Value") +

ylab("predicted value of log Median House")

8.4 Bagging

The tree based models given by CART are easy to understand and implement, but they suffer from high variance. That is, if we split the training data into two parts at random and fit a decision tree to both halves, the results that we get could be quite different (you might have seen this in your homework assignment!). We’d like a model that produces low variance - one for which if we ran it on different datasets, we’d get (close to) the same model every time.

Bagging = Bootstrap Aggregating. The idea is that sometimes when you fit multiple models and aggregate those models together, you get a smoother model fit which will give you a better balance between bias in your fit and variance in your fit. Bagging can be applied to any classifier to reduce variability.

Recall that the variance of the sample mean is variance of data / n. So we’ve seen the idea that averaging an outcome gives reduced variability.

8.4.1 Bagging algorithm

Algorithm: Bagging Forest

- Resample (bootstrap) cases (observational units, not variables).

- Build a tree on each new set of (bootstrapped) training observations.

- Average (regression) or majority vote (classification).

- Note that for every bootstrap sample, approximately 2/3 of the observations will be chosen and 1/3 of them will not be chosen.

\[\begin{align} P(\mbox{observation $i$ is not in the bootstrap sample}) &= \bigg(1 - \frac{1}{n} \bigg)^n\\ \lim_{n \rightarrow \infty} \bigg(1 - \frac{1}{n} \bigg)^n = \frac{1}{e} \approx \frac{1}{3} \end{align}\]

Shortcomings of Bagging:

- Model is even harder to “write-down” (than CART)

- With lots of predictors, (even greedy) partitioning can become computationally unwieldy - now computational task is even harder! (because of the number of trees grown for each bootstrap sample)

Strengths of Bagging:

- Can handle categorical or numerical predictors or response variables (indeed, they can handle mixed predictors at the same time!).

- Can handle more than 2 groups for categorical predictions

- Easily ignore redundant variables.

- Perform better than linear models in non-linear settings. Classification trees are non-linear models, so they immediately use interactions between variables.

- Data transformations may be less important (monotone transformations on the explanatory variables won’t change anything).

Similar bias to CART, but reduced variance

(can be proved).

Notes on bagging:

- Bagging alone uses the full set of predictors to determine every tree (it is the observations that are bootstrapped).

- Note that to predict for a particular observation, we start at the top, walk down the tree, and get the prediction. We average (or majority vote) the predictions to get one prediction for the observation at hand.

- Bagging gives a smoother decision boundary

- Bagging can be done on any decision method (not just trees).

- No need to prune or CV trees. The reason is that averaging keeps us from overfitting a particular few observations (think of averages in other contexts: law of large numbers). Pruning wouldn’t be a bad thing to do in terms of fit, but it is unnecessary for good predictions (and would add a lot to the complexity of the algorithm).

8.4.2 Out Of Bag (OOB) error rate

Additionally, with bagging, there is no need for cross-validation or a separate test set to get an unbiased estimate of the test set error. It is estimated internally, during the run, as follows:

- Each tree is constructed using a different bootstrap sample from the original data. About one-third of the cases are left out of the bootstrap sample and not used in the construction of the \(b^{th}\) tree.

- Put each case left out in the construction of the \(b^{th}\) tree down the \(b^{th}\) tree to get a classification. In this way, a test set classification is obtained for each case in about one-third of the trees.

- At the end of the run, take \(j\) to be the class that got most of the votes every time case \(i\) was oob. The proportion of times that \(j\) is not equal to the true class of n averaged over all cases is the oob error estimate. This has proven to be unbiased in many tests.

How does it work? Consider the following predictions for a silly toy data set of 9 observations. Recall that \(\sim 1/3\) of the observations will be left out at each bootstrap sample. Those are the observations for which predictions will be made. In the table below, an X is given if there is a prediction made for that value.

| obs | tree1 | tree2 | tree3 | tree4 | \(\cdots\) | tree100 | average |

|---|---|---|---|---|---|---|---|

| 1 | X | X | \(\sum(pred)/38\) | ||||

| 2 | X | \(\sum(pred)/30\) | |||||

| 3 | X | X | \(\sum(pred)/33\) | ||||

| 4 | X | \(\sum(pred)/32\) | |||||

| 5 | X | \(\sum(pred)/39\) | |||||

| 6 | X | X | \(\sum(pred)/29\) | ||||

| 7 | X | \(\sum(pred)/29\) | |||||

| 8 | X | X | X | \(\sum(pred)/31\) | |||

| 9 | X | \(\sum(pred)/36\) |

Let the OOB prediction for the \(i^{th}\) observation to be \(\hat{y}_{(-i)}\)

\[\begin{align} \mbox{OOB}_{\mbox{error}} &= \frac{1}{n} \sum_{i=1}^n \textrm{I} (y_i \ne \hat{y}_{(-i)}) \ \ \ \ \ \ \ \ \mbox{classification}\\ \mbox{OOB}_{\mbox{error}} &= \frac{1}{n} \sum_{i=1}^n (y_i - \hat{y}_{(-i)})^2 \ \ \ \ \ \ \ \ \mbox{regression}\\ \end{align}\]

8.5 Random Forests

Random Forests are an extension to bagging for regression trees (note: bagging can be done on any prediction method). Again, with the idea of infusing extra variability and then averaging over that variability, RFs use a subset of predictor variables at every node in the tree.

“Random forests does not overfit. You can run as many trees as you want.” Brieman, http://www.stat.berkeley.edu/~breiman/RandomForests/cc_home.htm

8.5.1 Random Forest algorithm

Algorithm: Random Forest

- Bootstrap sample from the training set.

- Grow an un-pruned tree on the bootstrap sample.

- At each split, select \(m\) variables and determine the best split using only the \(m\) predictors. Typically \(m = \sqrt{p}\) or \(\log_2 p\), where \(p\) is the number of features. Random Forests are not overly sensitive to the value of \(m\). [splits are chosen as with trees: according to either squared error or gini index / cross entropy / classification error.]

- Do not prune the tree. Save the tree as is!

- Repeat steps 1-2 for many many trees.

- For each tree grown on a bootstrap sample, predict the OOB samples. For each tree grown, \(~1/3\) of the training samples won’t be in the bootstrap sample – those are called out of bootstrap (OOB) samples. OOB samples can be used as test data to estimate the error rate of the tree.

- Combine the OOB predictions to create the “out-of-bag” error rate (either majority vote or average of predictions / class probabilities).

- All trees together represent the model that is used for new predictions (either majority vote or average).

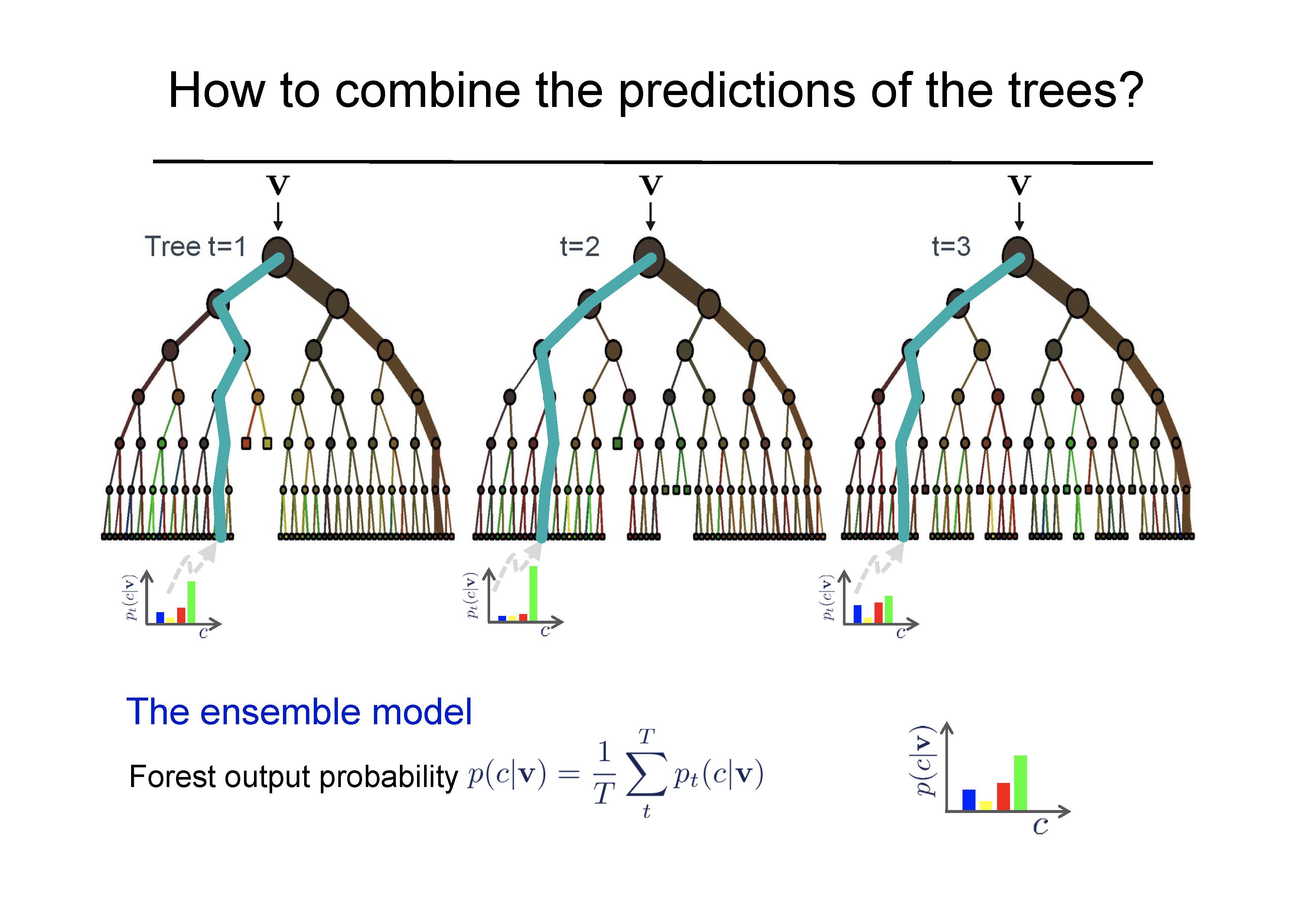

Figure 8.15: Building multiple trees and then combining the outputs (predictions). Note that this image makes the choice to average the tree probabilities instead of using majority vote. Both are valid methods for creating a Random Forest prediction model. http://www.robots.ox.ac.uk/~az/lectures/ml/lect4.pdf

Shortcomings of Random Forests:

- Model is even harder to “write-down” (than CART)

- With lots of predictors, (even greedy) partitioning can become computationally unwieldy - now computational task is even harder! … bagging the observations and

Strengths of Random Forests:

- refinement of bagged trees; quite popular (Random Forests tries to improve on bagging by “de-correlating” the trees. Each tree has the same expectation, but the average will again reduce the variability.)

- subset of predictors makes Random Forests much faster to search through than all predictors

- creates a diverse set of trees that can be built. Note that by bootstrapping the samples and the predictor variables, we add another level of randomness over which we can average to again decrease the variability.

- Random Forests are quite accurate

- generally, models do not overfit the data and CV is not needed. However, CV can be used to fit the tuning parameters (\(m\), node size, max number of nodes, etc.).

Notes on Random Forests:

- Bagging alone uses the full set of predictors to determine every tree (it is the observations that are bootstrapped). Random Forests use a subset of predictors.

- Note that to predict for a particular observation, we start at the top, walk down the tree, and get the prediction. We average (or majority vote) the predictions to get one prediction for the observation at hand.

- Bagging is a special case of Random Forest where \(m=p\).

- generally, models do not overfit the data and CV is not needed. However, CV can be used to fit the tuning parameters (\(m\), node size, max number of nodes, etc.).

“Random forests does not overfit. You can run as many trees as you want.” Brieman, http://www.stat.berkeley.edu/~breiman/RandomForests/cc_home.htm

How to choose parameters?

- \(\#\) trees Build trees until the error no longer decreases

- \(m\) Try the recommended defaults, half of them, and twice of them - pick the best (use CV to avoid overfitting).

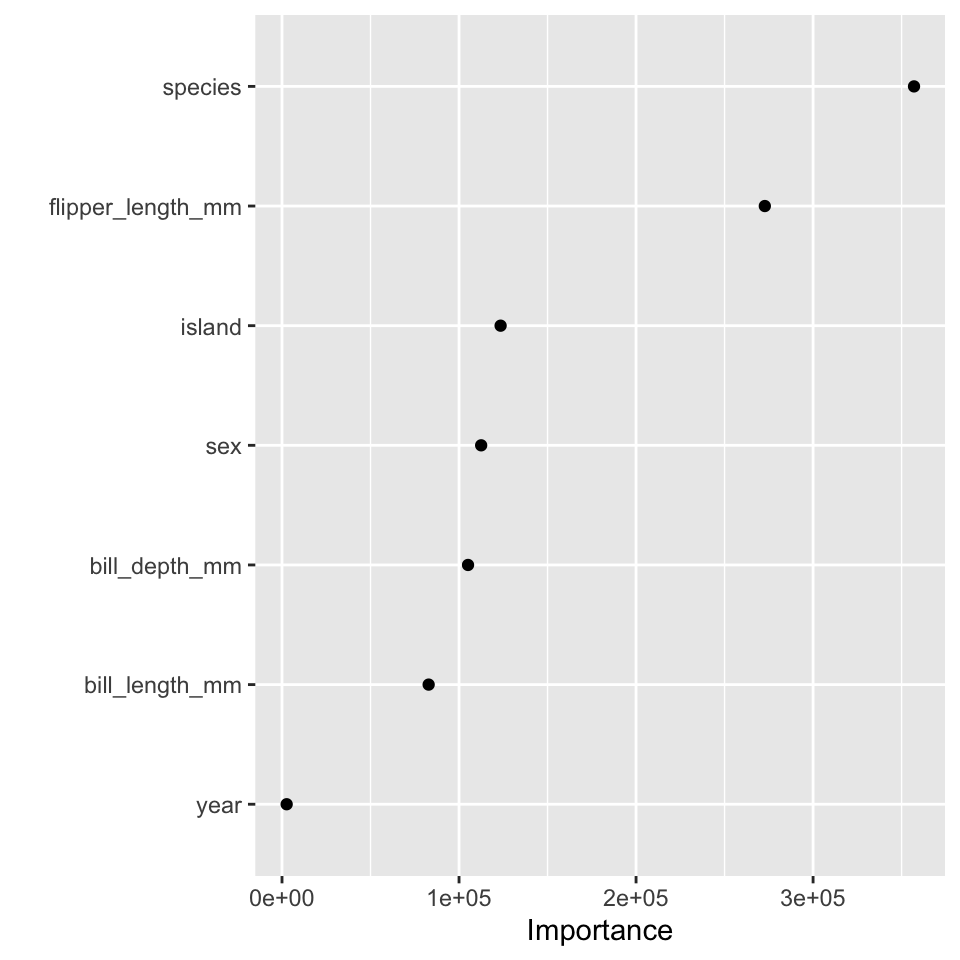

Variable Importance

All learners are bad when there are too many noisy variables because the response is bound to correlate with some of them. We can measure the contribution of each additional variable in the model by how much the model accuracy decreased when the given variable was excluded from the model.

importance = decrease in node impurity resulting from splits over that variable, averaged over all trees

(“impurity” is defined as RSS for regression trees and deviance for classification trees).

Variable importance is measured by two different metrics (from R help on importance):

- (permutation) accuracy: For each tree, the prediction error on the out-of-bag portion of the data is recorded (error rate for classification, MSE for regression).Permute the \(j^{th}\) variable and recalculate the prediction error. The difference between the two are then averaged over all trees (for the \(j^{th}\) variable) to give the importance for the \(j^{th}\) variable.

- purity: The decrease (or increase, depending on the plot) in node purity: root sum of squares (RSS) [deviance/gini for classification trees]. That is, the amount of total decrease in RSS from splitting on that variable, averaged over all trees.

If the number of variables is very large, forests can be run once with all the variables, then run again using only the most important variables from the first run.

8.5.2 R RF Example

(“impurity” is defined as RSS for regression trees and deviance for classification trees).

method= 'ranger' is about a zillion times faster than method = 'randomForest' or method = 'rf', but they all do the work.

library(tidymodels)

library(palmerpenguins)

data(penguins)

penguins <- penguins %>%

drop_na()

# partition

set.seed(47)

penguin_split <- initial_split(penguins)

penguin_train <- training(penguin_split)

penguin_test <- testing(penguin_split)

# recipe

penguin_rf_recipe <-

recipe(body_mass_g ~ . ,

data = penguin_train) %>%

step_unknown(sex, new_level = "unknown") %>%

step_mutate(year = as.factor(year))

#model

penguin_rf <- rand_forest(mtry = tune(),

trees = tune()) %>%

set_engine("ranger", importance = "permutation") %>%

set_mode("regression")

# workflow

penguin_rf_wflow <- workflow() %>%

add_model(penguin_rf) %>%

add_recipe(penguin_rf_recipe)

# CV

set.seed(234)

penguin_folds <- vfold_cv(penguin_train,

v = 4)

# parameters

penguin_grid <- grid_regular(mtry(range = c(2,7)),

trees(range = c(1,500)),

levels = 5)

# tune

penguin_rf_tune <-

penguin_rf_wflow %>%

tune_grid(resamples = penguin_folds,

grid = penguin_grid)

select_best(penguin_rf_tune, "rmse")## # A tibble: 1 × 3

## mtry trees .config

## <int> <int> <chr>

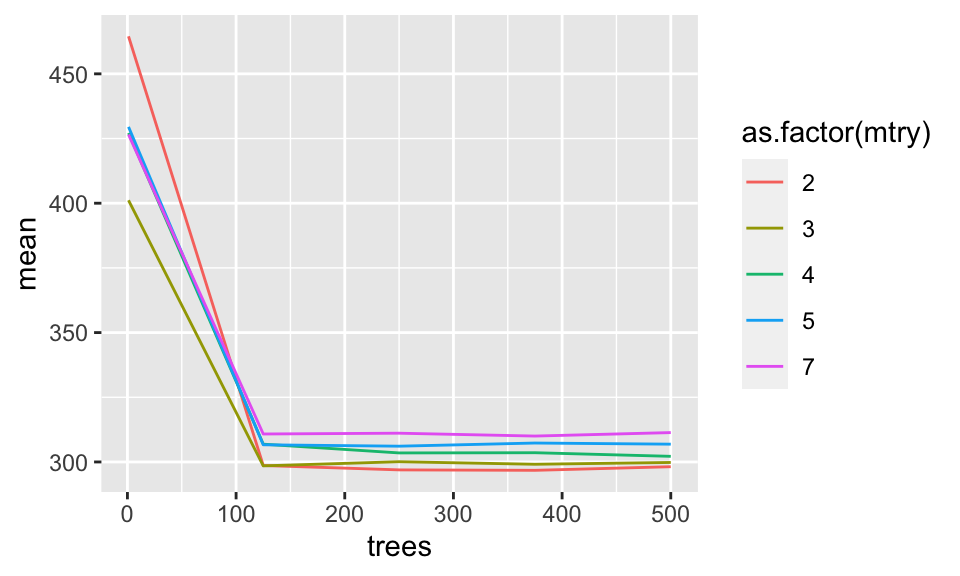

## 1 2 375 Preprocessor1_Model16Which mtry and number of trees?

penguin_rf_tune %>%

collect_metrics() %>%

filter(.metric == "rmse") %>%

ggplot() +

geom_line(aes(x = trees, y = mean, color = as.factor(mtry)))

Get the final model:

penguin_rf_best <- finalize_model(

penguin_rf,

select_best(penguin_rf_tune, "rmse"))

penguin_rf_best## Random Forest Model Specification (regression)

##

## Main Arguments:

## mtry = 2

## trees = 375

##

## Engine-Specific Arguments:

## importance = permutation

##

## Computational engine: ranger

penguin_rf_final <-

workflow() %>%

add_model(penguin_rf_best) %>%

add_recipe(penguin_rf_recipe) %>%

fit(data = penguin_train)

penguin_rf_final## ══ Workflow [trained] ══════════════════════════════════════════════════════════

## Preprocessor: Recipe

## Model: rand_forest()

##

## ── Preprocessor ────────────────────────────────────────────────────────────────

## 2 Recipe Steps

##

## • step_unknown()

## • step_mutate()

##

## ── Model ───────────────────────────────────────────────────────────────────────

## Ranger result

##

## Call:

## ranger::ranger(x = maybe_data_frame(x), y = y, mtry = min_cols(~2L, x), num.trees = ~375L, importance = ~"permutation", num.threads = 1, verbose = FALSE, seed = sample.int(10^5, 1))

##

## Type: Regression

## Number of trees: 375

## Sample size: 249

## Number of independent variables: 7

## Mtry: 2

## Target node size: 5

## Variable importance mode: permutation

## Splitrule: variance

## OOB prediction error (MSE): 84149.09

## R squared (OOB): 0.8634591Predict the test data:

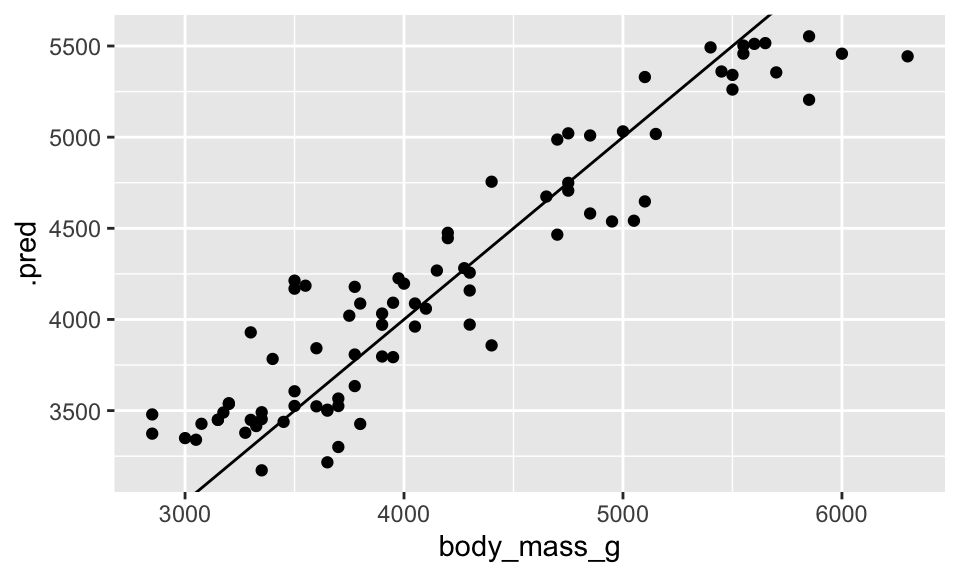

penguin_rf_final %>%

predict(new_data = penguin_test) %>%

cbind(penguin_test) %>%

ggplot() +

geom_point(aes(x = body_mass_g, y = .pred)) +

geom_abline(intercept = 0, slope = 1)

8.6 Model Choices

There are soooooo many choices we’ve made along the way. The following list should make you realize that there is no truth with respect to any given model. Every choice will (could) lead to a different model.

| \(\mbox{ }\) | \(\mbox{ }\) |

|---|---|

| * explanatory variable choice | * \(k\) (\(k\)-NN) |

| * number of explanatory variables | * distance measure |

| * functions/transformation of explanatory | * V (CV) |

| * transformation of response | * CV set.seed

|

| * response:continuous vs. categorical | * \(\alpha\) prune |

| * how missing data is dealt with | * maxdepth prune |

* train/test split (set.seed) |

* prune or not |

| * train/test proportion | * gini / entropy (split) |

| * type of classification model | * # trees / # BS samples |

| * use of cost complexity / parameter | * grid search etc. for tuning |

| * majority / average prob (tree error rate) | * value(s) of mtry

|

| * accuracy vs sensitivity vs specificity | * OOB vs CV for tuning |

8.7 Support Vector Machines

Support Vector Machines are one more algorithm for classification. As you’ll see, they have some excellent properties, but one important aspect to note is that they use only numeric predictor variables and only binary response variables (classify two groups).

Vladimir Vapnik (b. 1936) created SVMs in the late 1990s. History: he actually did the work as his PhD in the early 60s in the Soviet Union. Someone from Bell Labs asked him to visit, and he ended up immigrating to the US. No one actually thought that SVMs would work, but he eventually (1995 - took 30 years between the idea and the implementation) bet a dinner on classifying handwriting via SVM (using a very simple kernel) versus neural networks and the rest is history.

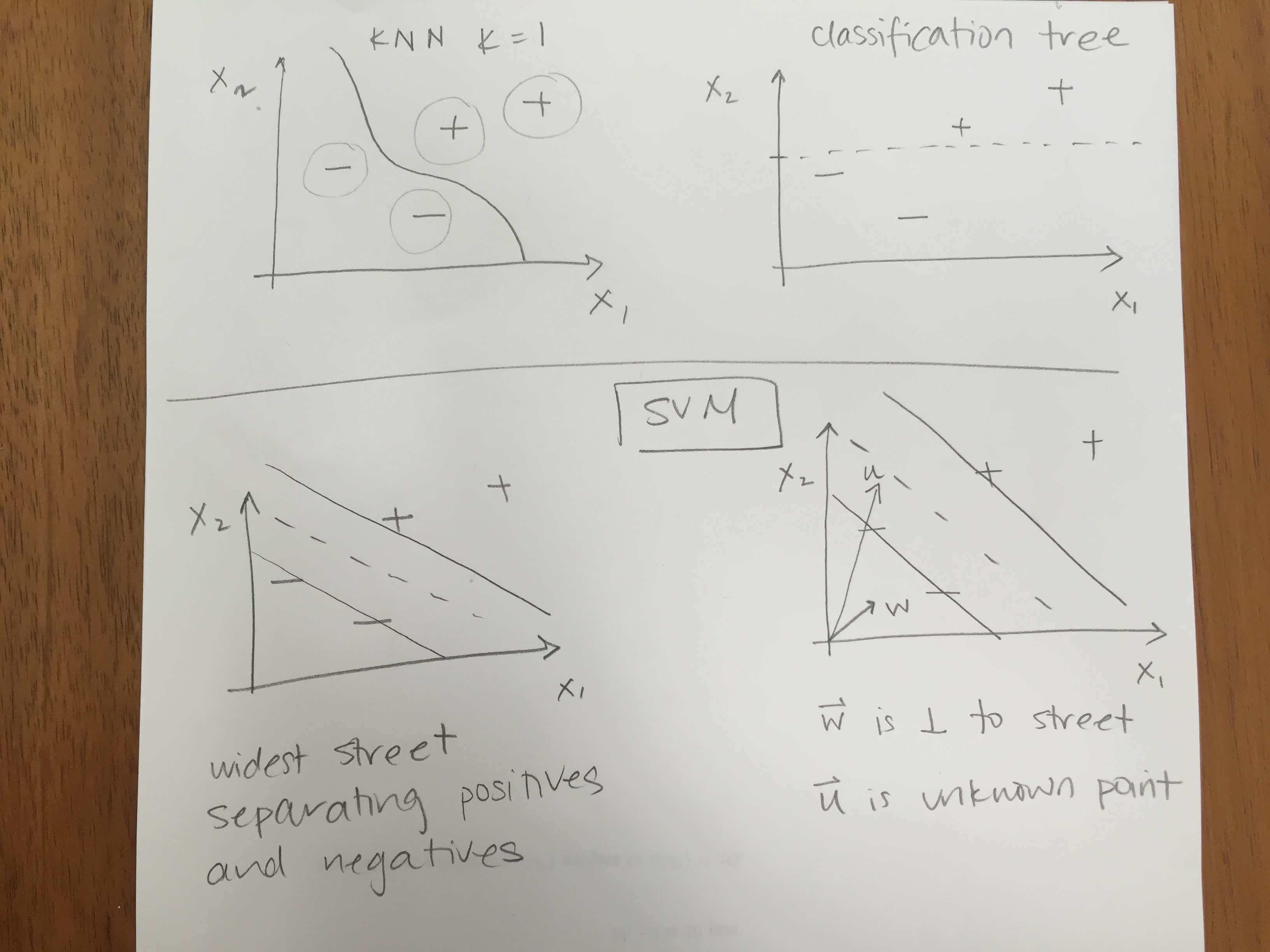

The basic idea of SVMs is to figure out a way to create really complicated decision boundaries. We want to put in a straight line with the widest possible street (draw street with gutters and 4 points, two positive and two negative). The decision rule has to do with a dot product of the new sample with a vector \({\bf w}\) which is perpendicular to the median of the “street.”

Note: the standard formulation of SVM requires the computer to find dot products between each of the observations. In order to do so, the explanatory variables must be numeric. In order for the dot products to be meaningful, the data must be on the same scale.

8.7.0.1 Linear Separator

Recall ideas of kNN and trees:

But today’s decision boundary is going to be based on a hyperplane which separates the values in the “best” way. Certainly, if the data are linearly separable, then there are infinitely many hyperplanes which will partition the data perfectly. For SVM, the idea is to find the “street” which separates the positive and negative samples to give the widest margin.

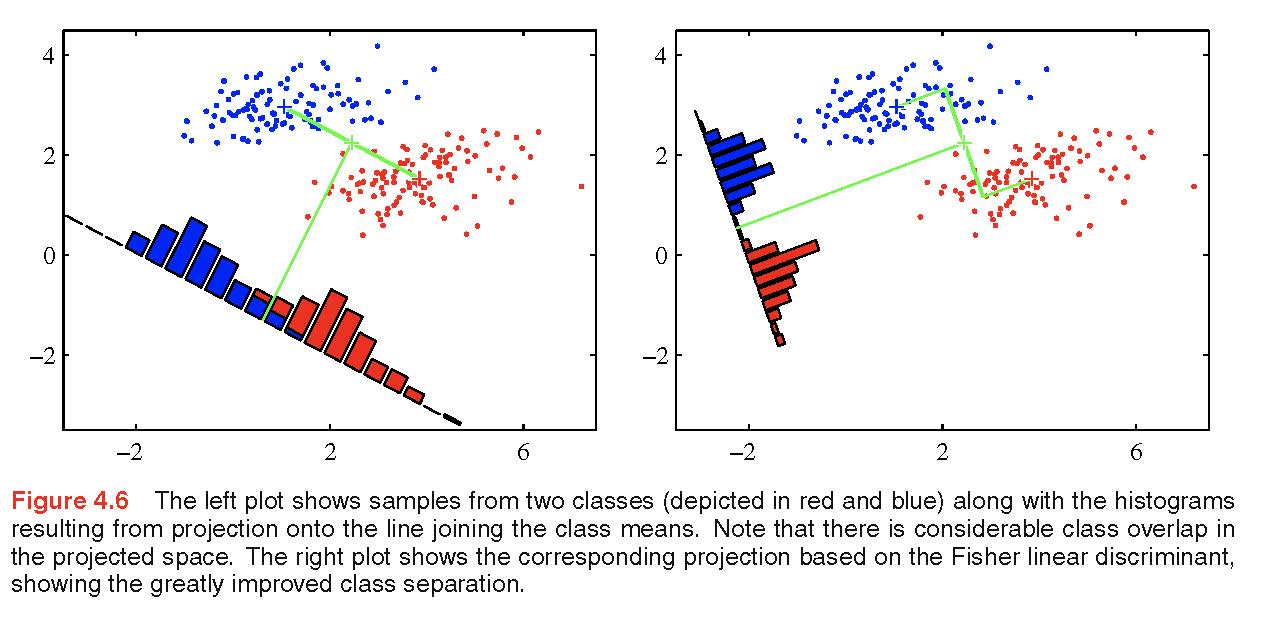

Figure 8.16: The correct project of the observations can often produce a perfect one dimensional (i.e., linear) classifier. http://www.rmki.kfki.hu/~banmi/elte/Bishop - Pattern Recognition and Machine Learning.pdf

Aside: what is a dot product?

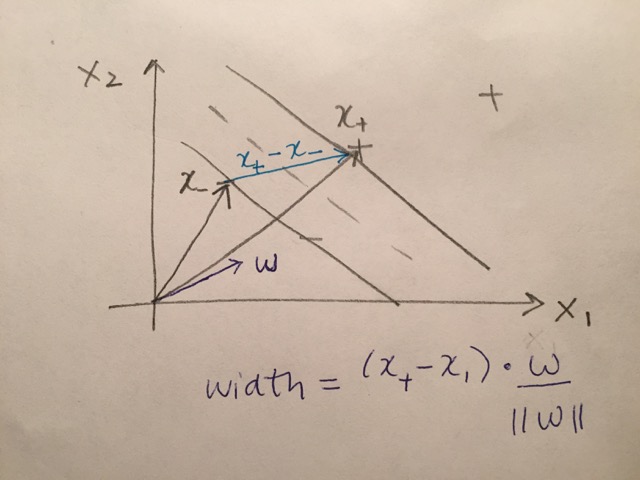

Let \({\bf x} = (x_1, x_2, \ldots, x_p)^t\) and \({\bf y} = (y_1, y_2, \ldots, y_p)^t\) be two vectors which live in \(R^p\). Then their dot product is defined as: \[\begin{align} {\bf x} \cdot {\bf y} = {\bf x}^t {\bf y} = \sum_{i=1}^p x_i y_i \end{align}\]

Figure 8.17: If w is known, then the projection of any new observation onto w will lead to a linear partition of the space.

How can the street be used to get a decision rule? All that is known is that \({\bf w}\) is perpendicular to the street. We don’t yet know \({\bf w}\) or \(b\).

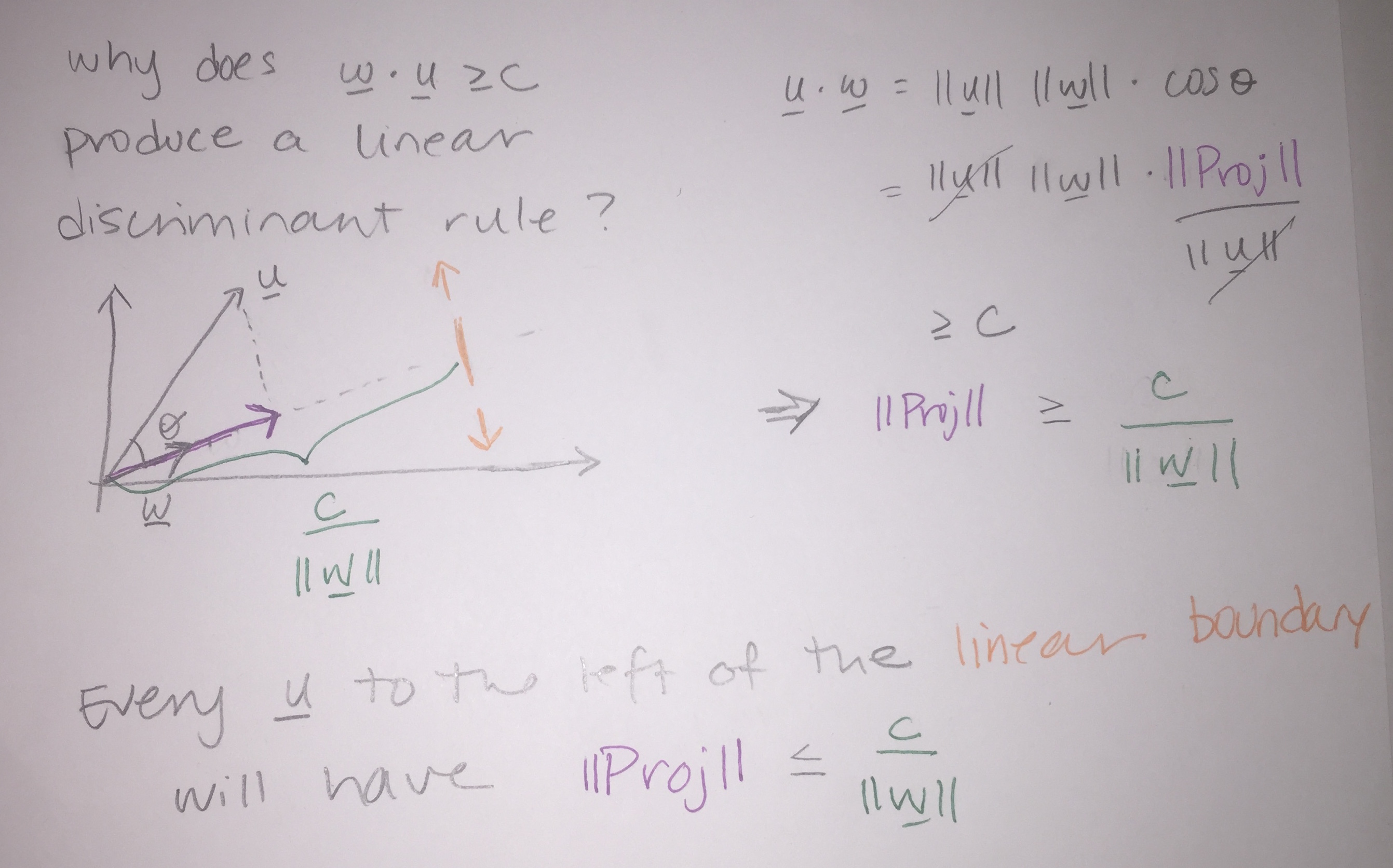

The “width” of the street will be a vector which is perpendicular to the street (median). We don’t know the width yet, but we know know that we can use that perpendicular vector (\({\bf w}\)) to figure out how to classify the points. Project an unknown point (\({\bf u}\)) onto \({\bf w}\) to see which side of the street the unknown value lands. That is, if the projection is large enough, we would classify the point as positive: \[{\bf w} \cdot {\bf u} \geq c?\]

[Keep in mind that \({\bf u} \cdot {\bf w} = ||{\bf w}|| \times\)(the length of the shadow). That is, the projection will only be the length of the shadow if \({\bf w}\) is a unit vector. And we aren’t going to constrain \({\bf w}\) to be unit vector (though we could!). But regardless, \({\bf u} \cdot {\bf w}\) still gives the ability to classify because it is proportional to the length of the shadow.]

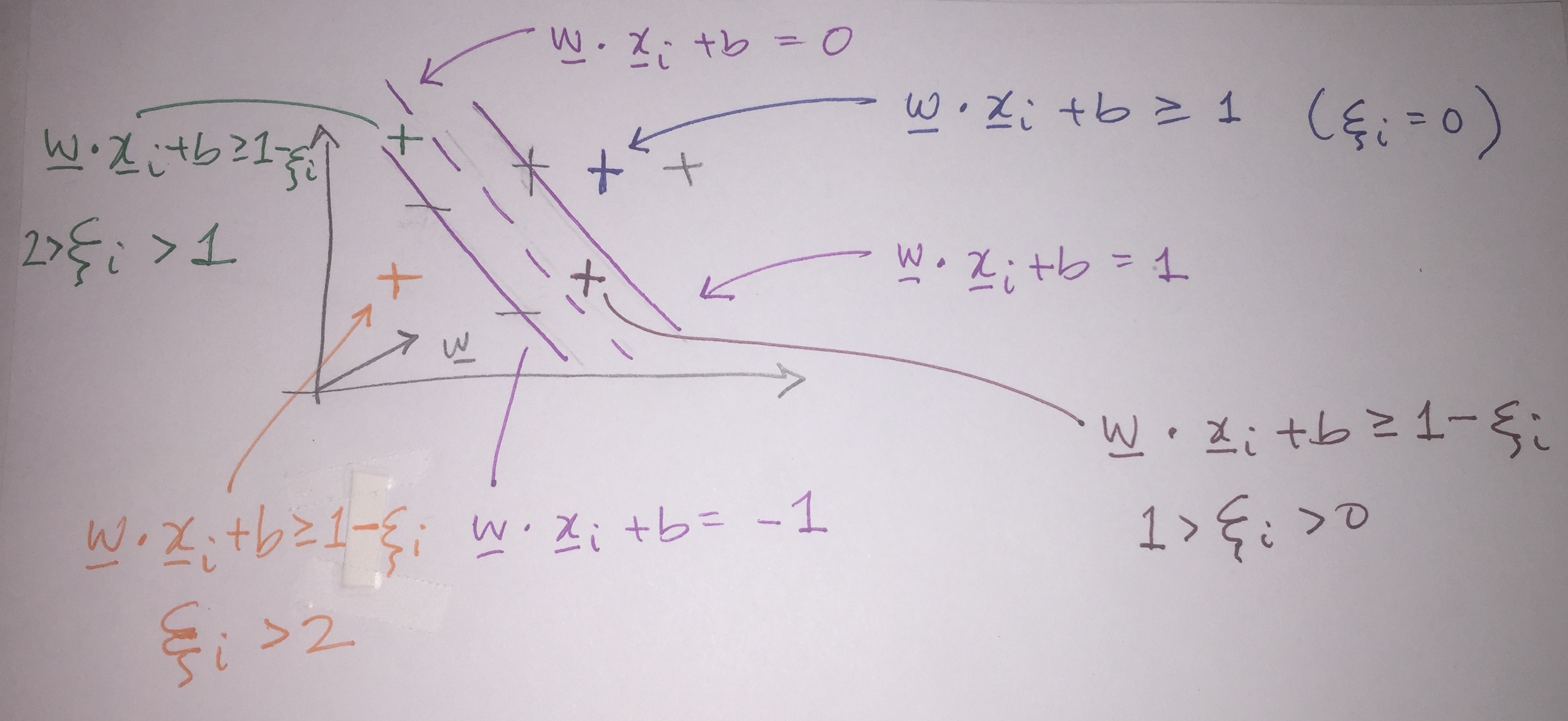

Decision rule: if \({\bf w} \cdot {\bf u} + b \geq 0\) then label the new sample “positive”

where \({\bf w}\) is created in such a way that it is perpendicular to the median of the street. Then the unknown (\({\bf u}\)) vector is projected onto \({\bf w}\) to see if it is on the left or the right side of the street.

But we don’t know the values in the decision rule! We need more constraints. Assuming that the data are linearly separable, as an initial step to find \({\bf w}\) and \(b\), for all positive samples (\(x_+\)) and all negative samples (\(x_-\)) force: \[\begin{align} {\bf w} \cdot {\bf x}_+ + b &\geq 1 \tag{8.1}\\ {\bf w} \cdot {\bf x}_- + b &\leq -1 \tag{8.2} \end{align}\]

For mathematical convenience (so that we don’t have 2 equations hanging around), introduce \(y_i\) such that \[\begin{align} y_i &= 1 \mbox{ for positive samples}\\ y_i &= -1 \mbox{ for negative samples} \end{align}\]

Which simplifies the criteria for finding \({\bf w}\) and \(b\) to be: \[ y_i({\bf w} \cdot {\bf x}_i + b) \geq 1\] (Multiplying through by -1 on equation ((8.2) switches the signs, and both equation ((8.1)) and ((8.2) end up as the same for both types of points.)

Again, working toward solving for \({\bf w}\) and \(b\), add the additional constraint that for the points in the gutter (on the margin lines):

For \(x_i\) in the gutter (by definition): \[y_i({\bf w} \cdot {\bf x}_i + b) - 1 = 0\]

Now consider two particular positive and negative values that live on the margin (gutter). The difference is almost the width of the street (we want to find the street that is as wide as possible), but it is at the wrong angle (see street picture again). Remember, our goal here is to find the street separating the pluses and the minuses that is as wide as possible. If we had a unit vector, we could dot it with \((x_+ - x_-)\) to get the width of the street!

\[\begin{align} width = \frac{(x_+ - x_-) \cdot {\bf w}}{|| {\bf w} ||} \end{align}\] which doesn’t do us much good yet.

Goal: Try to find as wide a street as possible.

But remember, the gutter points are constrained: it turns out that \(x_+ \cdot {\bf w} = 1 - b\) and \(x_- \cdot {\bf w} = -1 - b\). Therefore:

\[\begin{align} width = \frac{(x_+ - x_-) \cdot {\bf w}}{|| {\bf w} ||} = \frac{(1-b) - (-1-b)}{|| {\bf w} ||} = \frac{2}{||w||} \end{align}\]

In order to maximize \(\frac{2}{||w||}\), minimize \(||w||\), orminimize \((1/2)*||w||^2\)

(to make it mathematically easier). We have all the pieces of making the decision rules as an optimization problem. That is, minimize some quantity subject to the constraints given by the problem.

Lagrange multipliers

Recall, with Lagrange multipliers, the first part is the optimization, the second part is the constraint. The point of Lagrange multipliers is to put together the constraint and the optimization into one equation where you don’t worry about the constraints any longer.